{"title":"目标日期基金的业绩分散性","authors":"Ivelina Pavlova, Ann Marie Hibbert","doi":"10.1057/s41260-024-00349-0","DOIUrl":null,"url":null,"abstract":"<p>There are significant differences in the performance of Target Date Funds (TDFs) with the same target year. Using a unique dataset from Morningstar, we show that within the same target year, funds with lower than the average expense ratio, or higher than average allocation to equities, outperform similar funds. This outperformance exists across all target year groups and is economically meaningful. Furthermore, deviations in the equity allocation have a greater impact on performance than does expense ratio. Using bootstrap simulations to investigate the impact over a longer horizon, we show that deviations from the average allocations or expense ratios have a meaningful impact on the retirement savings of an average investor.</p>","PeriodicalId":45953,"journal":{"name":"Journal of Asset Management","volume":"43 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2024-02-24","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Performance dispersion among target date funds\",\"authors\":\"Ivelina Pavlova, Ann Marie Hibbert\",\"doi\":\"10.1057/s41260-024-00349-0\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>There are significant differences in the performance of Target Date Funds (TDFs) with the same target year. Using a unique dataset from Morningstar, we show that within the same target year, funds with lower than the average expense ratio, or higher than average allocation to equities, outperform similar funds. This outperformance exists across all target year groups and is economically meaningful. Furthermore, deviations in the equity allocation have a greater impact on performance than does expense ratio. Using bootstrap simulations to investigate the impact over a longer horizon, we show that deviations from the average allocations or expense ratios have a meaningful impact on the retirement savings of an average investor.</p>\",\"PeriodicalId\":45953,\"journal\":{\"name\":\"Journal of Asset Management\",\"volume\":\"43 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2024-02-24\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Asset Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1057/s41260-024-00349-0\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Asset Management","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41260-024-00349-0","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

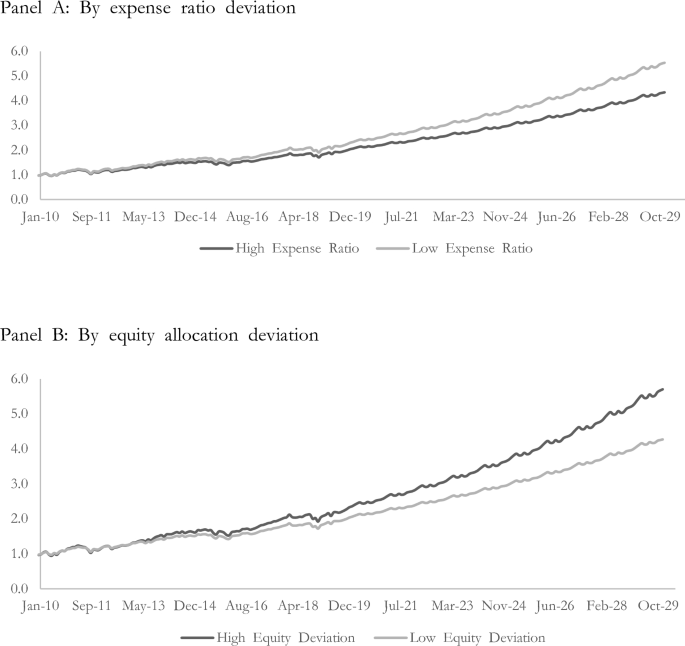

There are significant differences in the performance of Target Date Funds (TDFs) with the same target year. Using a unique dataset from Morningstar, we show that within the same target year, funds with lower than the average expense ratio, or higher than average allocation to equities, outperform similar funds. This outperformance exists across all target year groups and is economically meaningful. Furthermore, deviations in the equity allocation have a greater impact on performance than does expense ratio. Using bootstrap simulations to investigate the impact over a longer horizon, we show that deviations from the average allocations or expense ratios have a meaningful impact on the retirement savings of an average investor.

期刊介绍:

The Journal of Asset Management covers:new investment strategies, methodologies and techniquesnew products and trading developmentsimportant regulatory and legal developmentsemerging trends in asset managementUnder the guidance of its expert Editors and an eminent international Editorial Board, Journal of Asset Management has developed to provide an international forum for latest thinking, techniques and developments for the Fund Management Industry, from high-growth investment strategies to modelling and managing risk, from active management to index tracking. The Journal has established itself as a key bridge between applied academic research, commercial best practice and regulatory interests, globally.Each issue of Journal of Asset Management publishes detailed, authoritative briefings, analysis, research and reviews by leading experts in the field, to keep subscribers up to date with the latest developments and thinking in asset management.Journal of Asset Management covers:asset allocation hedge fund strategies risk definition and management index tracking performance measurement stock selection investment methodologies and techniques portfolio management and weighting product development and innovation active asset management style analysis strategies to match client profiles time horizons emerging markets alternative investments derivatives and hedging instruments pensions economics

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们