{"title":"数字化与跨境税务欺诈:意大利电子发票的证据","authors":"Marwin Heinemann, Wojciech Stiller","doi":"10.1007/s10797-023-09820-x","DOIUrl":null,"url":null,"abstract":"<p>The digitalization of transaction processes through tools such as electronic invoicing (e-invoicing) aims to improve tax compliance and reduce administrative costs. Another important aspect of digitalization is its potential to reduce tax fraud. We exploit the comprehensive introduction of e-invoicing in Italy in 2019 and examine the effect of increased domestic tax enforcement capabilities on cross-border value-added tax (VAT) fraud. As a proxy for this fraud, we make use of the discrepancy in trade data that are double-reported in both the importing and exporting country (trade data gap, TDG). We calculate the TDG for imports to Italy from all other EU countries at the most detailed product level. Our results suggest a significant decline in cross-border fraud in response to the introduction of mandatory e-invoicing, providing an important rationale for the application of this measure by other countries. Furthermore, we estimate that e-invoicing decreased the Italian VAT loss in 2019 by about € 2.2 billion to € 2.6 billion compared to 2018. In this context, we underpin the suitability of the TDG as an approach for the study of anti-fraud measures.</p>","PeriodicalId":47518,"journal":{"name":"International Tax and Public Finance","volume":"111 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2024-02-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Digitalization and cross-border tax fraud: evidence from e-invoicing in Italy\",\"authors\":\"Marwin Heinemann, Wojciech Stiller\",\"doi\":\"10.1007/s10797-023-09820-x\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The digitalization of transaction processes through tools such as electronic invoicing (e-invoicing) aims to improve tax compliance and reduce administrative costs. Another important aspect of digitalization is its potential to reduce tax fraud. We exploit the comprehensive introduction of e-invoicing in Italy in 2019 and examine the effect of increased domestic tax enforcement capabilities on cross-border value-added tax (VAT) fraud. As a proxy for this fraud, we make use of the discrepancy in trade data that are double-reported in both the importing and exporting country (trade data gap, TDG). We calculate the TDG for imports to Italy from all other EU countries at the most detailed product level. Our results suggest a significant decline in cross-border fraud in response to the introduction of mandatory e-invoicing, providing an important rationale for the application of this measure by other countries. Furthermore, we estimate that e-invoicing decreased the Italian VAT loss in 2019 by about € 2.2 billion to € 2.6 billion compared to 2018. In this context, we underpin the suitability of the TDG as an approach for the study of anti-fraud measures.</p>\",\"PeriodicalId\":47518,\"journal\":{\"name\":\"International Tax and Public Finance\",\"volume\":\"111 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2024-02-28\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Tax and Public Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10797-023-09820-x\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Tax and Public Finance","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10797-023-09820-x","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Digitalization and cross-border tax fraud: evidence from e-invoicing in Italy

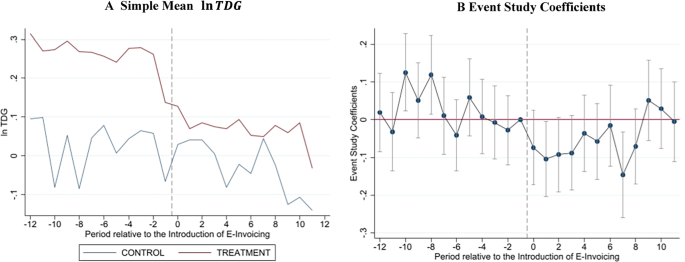

The digitalization of transaction processes through tools such as electronic invoicing (e-invoicing) aims to improve tax compliance and reduce administrative costs. Another important aspect of digitalization is its potential to reduce tax fraud. We exploit the comprehensive introduction of e-invoicing in Italy in 2019 and examine the effect of increased domestic tax enforcement capabilities on cross-border value-added tax (VAT) fraud. As a proxy for this fraud, we make use of the discrepancy in trade data that are double-reported in both the importing and exporting country (trade data gap, TDG). We calculate the TDG for imports to Italy from all other EU countries at the most detailed product level. Our results suggest a significant decline in cross-border fraud in response to the introduction of mandatory e-invoicing, providing an important rationale for the application of this measure by other countries. Furthermore, we estimate that e-invoicing decreased the Italian VAT loss in 2019 by about € 2.2 billion to € 2.6 billion compared to 2018. In this context, we underpin the suitability of the TDG as an approach for the study of anti-fraud measures.

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们