{"title":"针对私人逐国报告的监管规避对策","authors":"Felix Hugger","doi":"10.1007/s10797-024-09827-y","DOIUrl":null,"url":null,"abstract":"<p>This paper investigates regulatory avoidance in the context of private country-by-country reporting (CbCR) introduced as part of the OECD/G20 BEPS initiative. The reporting framework requires multinational companies above a revenue threshold to provide tax authorities with new and detailed information on their global activities, but the data are not made publicly available. I find robust evidence for an increase in mass below the revenue threshold after the introduction of CbCR in line with an avoidance response. Company types for which CbCR would imply relatively high costs including private companies or more tax-aggressive firms show a stronger avoidance response. The heterogeneities found can at least partially be explained by an analysis of increases in tax costs. The finding of regulatory avoidance of multinational enterprises in response to a fixed revenue threshold is of additional relevance in light of the international tax reform agenda which relies on similar thresholds.</p>","PeriodicalId":47518,"journal":{"name":"International Tax and Public Finance","volume":"69 1","pages":""},"PeriodicalIF":1.4000,"publicationDate":"2024-03-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Regulatory avoidance responses to private Country-by-Country Reporting\",\"authors\":\"Felix Hugger\",\"doi\":\"10.1007/s10797-024-09827-y\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper investigates regulatory avoidance in the context of private country-by-country reporting (CbCR) introduced as part of the OECD/G20 BEPS initiative. The reporting framework requires multinational companies above a revenue threshold to provide tax authorities with new and detailed information on their global activities, but the data are not made publicly available. I find robust evidence for an increase in mass below the revenue threshold after the introduction of CbCR in line with an avoidance response. Company types for which CbCR would imply relatively high costs including private companies or more tax-aggressive firms show a stronger avoidance response. The heterogeneities found can at least partially be explained by an analysis of increases in tax costs. The finding of regulatory avoidance of multinational enterprises in response to a fixed revenue threshold is of additional relevance in light of the international tax reform agenda which relies on similar thresholds.</p>\",\"PeriodicalId\":47518,\"journal\":{\"name\":\"International Tax and Public Finance\",\"volume\":\"69 1\",\"pages\":\"\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2024-03-13\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Tax and Public Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s10797-024-09827-y\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Tax and Public Finance","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s10797-024-09827-y","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Regulatory avoidance responses to private Country-by-Country Reporting

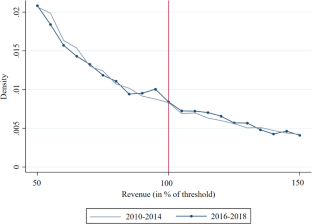

This paper investigates regulatory avoidance in the context of private country-by-country reporting (CbCR) introduced as part of the OECD/G20 BEPS initiative. The reporting framework requires multinational companies above a revenue threshold to provide tax authorities with new and detailed information on their global activities, but the data are not made publicly available. I find robust evidence for an increase in mass below the revenue threshold after the introduction of CbCR in line with an avoidance response. Company types for which CbCR would imply relatively high costs including private companies or more tax-aggressive firms show a stronger avoidance response. The heterogeneities found can at least partially be explained by an analysis of increases in tax costs. The finding of regulatory avoidance of multinational enterprises in response to a fixed revenue threshold is of additional relevance in light of the international tax reform agenda which relies on similar thresholds.

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们