{"title":"意大利每月运输周转量指标的间接估算","authors":"Barbara Guardabascio, Filippo Moauro, Luke Mosley","doi":"10.1007/s00181-024-02571-6","DOIUrl":null,"url":null,"abstract":"<p>The paper discusses the results of a selection of a set of monthly indicators to be used as predictors of the quarterly index of Italian service turnover. A mixed frequency approach based on sparse temporal disaggregation is used, which outperforms the classical methods of the Chow and Lin family, allowing both a high number of regressors by the LASSO method and stable estimates. The application refers to the turnover in transport, a sector strongly affected in 2020 by the dramatic movements due to the COVID-19 pandemic and the resurgence of inflation at the end of 2021. The monthly indicators are selected from 143 time series: 56 series of business surveys in transport about both the climate and frequency of the answers; 18 series from Assaeroporti about both passengers and cargo flights split by national and international routes; 69 series of monthly turnover in industry split by both sector of economic activity and reference market. The sample spans the months from January 2010 to December 2021 for both seasonally adjusted and unadjusted data. Several aspects of the estimation are considered: the stability of selected indicators over the quarters 2017–2021; their forecasting performance; the reliability of the estimates in terms of their monthly pattern.</p>","PeriodicalId":11642,"journal":{"name":"Empirical Economics","volume":"147 1","pages":""},"PeriodicalIF":1.9000,"publicationDate":"2024-03-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Indirect estimation of the monthly transport turnover indicator in Italy\",\"authors\":\"Barbara Guardabascio, Filippo Moauro, Luke Mosley\",\"doi\":\"10.1007/s00181-024-02571-6\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>The paper discusses the results of a selection of a set of monthly indicators to be used as predictors of the quarterly index of Italian service turnover. A mixed frequency approach based on sparse temporal disaggregation is used, which outperforms the classical methods of the Chow and Lin family, allowing both a high number of regressors by the LASSO method and stable estimates. The application refers to the turnover in transport, a sector strongly affected in 2020 by the dramatic movements due to the COVID-19 pandemic and the resurgence of inflation at the end of 2021. The monthly indicators are selected from 143 time series: 56 series of business surveys in transport about both the climate and frequency of the answers; 18 series from Assaeroporti about both passengers and cargo flights split by national and international routes; 69 series of monthly turnover in industry split by both sector of economic activity and reference market. The sample spans the months from January 2010 to December 2021 for both seasonally adjusted and unadjusted data. Several aspects of the estimation are considered: the stability of selected indicators over the quarters 2017–2021; their forecasting performance; the reliability of the estimates in terms of their monthly pattern.</p>\",\"PeriodicalId\":11642,\"journal\":{\"name\":\"Empirical Economics\",\"volume\":\"147 1\",\"pages\":\"\"},\"PeriodicalIF\":1.9000,\"publicationDate\":\"2024-03-19\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Empirical Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s00181-024-02571-6\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Empirical Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s00181-024-02571-6","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Indirect estimation of the monthly transport turnover indicator in Italy

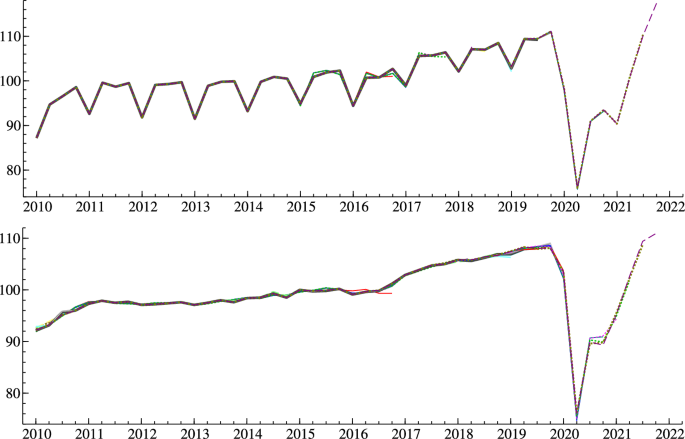

The paper discusses the results of a selection of a set of monthly indicators to be used as predictors of the quarterly index of Italian service turnover. A mixed frequency approach based on sparse temporal disaggregation is used, which outperforms the classical methods of the Chow and Lin family, allowing both a high number of regressors by the LASSO method and stable estimates. The application refers to the turnover in transport, a sector strongly affected in 2020 by the dramatic movements due to the COVID-19 pandemic and the resurgence of inflation at the end of 2021. The monthly indicators are selected from 143 time series: 56 series of business surveys in transport about both the climate and frequency of the answers; 18 series from Assaeroporti about both passengers and cargo flights split by national and international routes; 69 series of monthly turnover in industry split by both sector of economic activity and reference market. The sample spans the months from January 2010 to December 2021 for both seasonally adjusted and unadjusted data. Several aspects of the estimation are considered: the stability of selected indicators over the quarters 2017–2021; their forecasting performance; the reliability of the estimates in terms of their monthly pattern.

期刊介绍:

Empirical Economics publishes high quality papers using econometric or statistical methods to fill the gap between economic theory and observed data. Papers explore such topics as estimation of established relationships between economic variables, testing of hypotheses derived from economic theory, treatment effect estimation, policy evaluation, simulation, forecasting, as well as econometric methods and measurement. Empirical Economics emphasizes the replicability of empirical results. Replication studies of important results in the literature - both positive and negative results - may be published as short papers in Empirical Economics. Authors of all accepted papers and replications are required to submit all data and codes prior to publication (for more details, see: Instructions for Authors).The journal follows a single blind review procedure. In order to ensure the high quality of the journal and an efficient editorial process, a substantial number of submissions that have very poor chances of receiving positive reviews are routinely rejected without sending the papers for review.Officially cited as: Empir Econ

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们