{"title":"利用非观测变量模型区分收益的经常性和非经常性组成部分","authors":"","doi":"10.1016/j.jacceco.2024.101687","DOIUrl":null,"url":null,"abstract":"<div><p>Distinguishing between recurring and nonrecurring components of earnings is a critical task in financial analysis and valuation. Academics and quantitative investors often rely on measures of recurring and nonrecurring components derived from standardized financial databases. We use unobserved components modeling and the Kalman smoother to obtain efficient ex-post estimates of the recurring and nonrecurring components of annual earnings. We then show that popular measures are significantly misspecified and that investors appear to anticipate a significant portion of the misspecification. Finally, we identify certain misclassified items that drive misspecification and provide algorithms to improve their ex-ante classification.</p></div>","PeriodicalId":48438,"journal":{"name":"Journal of Accounting & Economics","volume":"78 1","pages":"Article 101687"},"PeriodicalIF":6.8000,"publicationDate":"2024-08-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Distinguishing between recurring and nonrecurring components of earnings using unobserved components modeling\",\"authors\":\"\",\"doi\":\"10.1016/j.jacceco.2024.101687\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>Distinguishing between recurring and nonrecurring components of earnings is a critical task in financial analysis and valuation. Academics and quantitative investors often rely on measures of recurring and nonrecurring components derived from standardized financial databases. We use unobserved components modeling and the Kalman smoother to obtain efficient ex-post estimates of the recurring and nonrecurring components of annual earnings. We then show that popular measures are significantly misspecified and that investors appear to anticipate a significant portion of the misspecification. Finally, we identify certain misclassified items that drive misspecification and provide algorithms to improve their ex-ante classification.</p></div>\",\"PeriodicalId\":48438,\"journal\":{\"name\":\"Journal of Accounting & Economics\",\"volume\":\"78 1\",\"pages\":\"Article 101687\"},\"PeriodicalIF\":6.8000,\"publicationDate\":\"2024-08-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Accounting & Economics\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://www.sciencedirect.com/science/article/pii/S016541012400017X\",\"RegionNum\":1,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2024/3/24 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Accounting & Economics","FirstCategoryId":"91","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S016541012400017X","RegionNum":1,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2024/3/24 0:00:00","PubModel":"Epub","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Distinguishing between recurring and nonrecurring components of earnings using unobserved components modeling

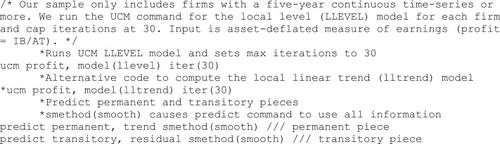

Distinguishing between recurring and nonrecurring components of earnings is a critical task in financial analysis and valuation. Academics and quantitative investors often rely on measures of recurring and nonrecurring components derived from standardized financial databases. We use unobserved components modeling and the Kalman smoother to obtain efficient ex-post estimates of the recurring and nonrecurring components of annual earnings. We then show that popular measures are significantly misspecified and that investors appear to anticipate a significant portion of the misspecification. Finally, we identify certain misclassified items that drive misspecification and provide algorithms to improve their ex-ante classification.

期刊介绍:

The Journal of Accounting and Economics encourages the application of economic theory to the explanation of accounting phenomena. It provides a forum for the publication of the highest quality manuscripts which employ economic analyses of accounting problems. A wide range of methodologies and topics are encouraged and covered: * The role of accounting within the firm; * The information content and role of accounting numbers in capital markets; * The role of accounting in financial contracts and in monitoring agency relationships; * The determination of accounting standards; * Government regulation of corporate disclosure and/or the Accounting profession; * The theory of the accounting firm.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们