{"title":"收入不确定情况下的生产灵活性和贸易信贷","authors":"Nicos Koussis, Florina Silaghi","doi":"10.1111/jbfa.12786","DOIUrl":null,"url":null,"abstract":"<p>In an uncertain economic environment, the ability of firms to adapt their production levels to unforeseen market demand is critical for their investment, financing and trade credit policies. This paper focuses on the impact of production flexibility on trade credit values and maturity in the presence of uncertain demand. We develop a continuous-time real options framework where a buyer firm with capacity constraints orders input goods on credit from a supplier. The supplier optimally chooses the trade credit maturity, considering its influence on the buyer's optimal quantities and default timing. We distinguish between flexible firms, capable of suspending production during adverse conditions, and rigid firms, constrained to constant full-scale production. Our findings reveal that production flexibility positively affects trade credit values and maturity. Flexible firms invest in larger capacity, default later and order larger quantities, resulting in higher trade credit values. Suppliers extend longer maturities to flexible firms, reflecting their higher creditworthiness and the positive effects of extended trade credit on their installed capacity. Furthermore, we explore extensions to our framework, including switching costs, entry timing, interactions between debt and trade credit and a non-cooperative bargaining game.</p>","PeriodicalId":48106,"journal":{"name":"Journal of Business Finance & Accounting","volume":"51 9-10","pages":"2371-2409"},"PeriodicalIF":2.4000,"publicationDate":"2024-01-28","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12786","citationCount":"0","resultStr":"{\"title\":\"Production flexibility and trade credit under revenue uncertainty\",\"authors\":\"Nicos Koussis, Florina Silaghi\",\"doi\":\"10.1111/jbfa.12786\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In an uncertain economic environment, the ability of firms to adapt their production levels to unforeseen market demand is critical for their investment, financing and trade credit policies. This paper focuses on the impact of production flexibility on trade credit values and maturity in the presence of uncertain demand. We develop a continuous-time real options framework where a buyer firm with capacity constraints orders input goods on credit from a supplier. The supplier optimally chooses the trade credit maturity, considering its influence on the buyer's optimal quantities and default timing. We distinguish between flexible firms, capable of suspending production during adverse conditions, and rigid firms, constrained to constant full-scale production. Our findings reveal that production flexibility positively affects trade credit values and maturity. Flexible firms invest in larger capacity, default later and order larger quantities, resulting in higher trade credit values. Suppliers extend longer maturities to flexible firms, reflecting their higher creditworthiness and the positive effects of extended trade credit on their installed capacity. Furthermore, we explore extensions to our framework, including switching costs, entry timing, interactions between debt and trade credit and a non-cooperative bargaining game.</p>\",\"PeriodicalId\":48106,\"journal\":{\"name\":\"Journal of Business Finance & Accounting\",\"volume\":\"51 9-10\",\"pages\":\"2371-2409\"},\"PeriodicalIF\":2.4000,\"publicationDate\":\"2024-01-28\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jbfa.12786\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Business Finance & Accounting\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12786\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Business Finance & Accounting","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jbfa.12786","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Production flexibility and trade credit under revenue uncertainty

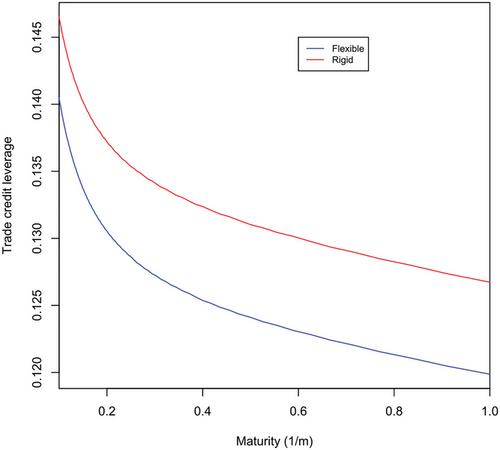

In an uncertain economic environment, the ability of firms to adapt their production levels to unforeseen market demand is critical for their investment, financing and trade credit policies. This paper focuses on the impact of production flexibility on trade credit values and maturity in the presence of uncertain demand. We develop a continuous-time real options framework where a buyer firm with capacity constraints orders input goods on credit from a supplier. The supplier optimally chooses the trade credit maturity, considering its influence on the buyer's optimal quantities and default timing. We distinguish between flexible firms, capable of suspending production during adverse conditions, and rigid firms, constrained to constant full-scale production. Our findings reveal that production flexibility positively affects trade credit values and maturity. Flexible firms invest in larger capacity, default later and order larger quantities, resulting in higher trade credit values. Suppliers extend longer maturities to flexible firms, reflecting their higher creditworthiness and the positive effects of extended trade credit on their installed capacity. Furthermore, we explore extensions to our framework, including switching costs, entry timing, interactions between debt and trade credit and a non-cooperative bargaining game.

期刊介绍:

Journal of Business Finance and Accounting exists to publish high quality research papers in accounting, corporate finance, corporate governance and their interfaces. The interfaces are relevant in many areas such as financial reporting and communication, valuation, financial performance measurement and managerial reward and control structures. A feature of JBFA is that it recognises that informational problems are pervasive in financial markets and business organisations, and that accounting plays an important role in resolving such problems. JBFA welcomes both theoretical and empirical contributions. Nonetheless, theoretical papers should yield novel testable implications, and empirical papers should be theoretically well-motivated. The Editors view accounting and finance as being closely related to economics and, as a consequence, papers submitted will often have theoretical motivations that are grounded in economics. JBFA, however, also seeks papers that complement economics-based theorising with theoretical developments originating in other social science disciplines or traditions. While many papers in JBFA use econometric or related empirical methods, the Editors also welcome contributions that use other empirical research methods. Although the scope of JBFA is broad, it is not a suitable outlet for highly abstract mathematical papers, or empirical papers with inadequate theoretical motivation. Also, papers that study asset pricing, or the operations of financial markets, should have direct implications for one or more of preparers, regulators, users of financial statements, and corporate financial decision makers, or at least should have implications for the development of future research relevant to such users.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们