{"title":"美国叙事税变革对产出、就业和价格的影响:因子增强向量自回归方法","authors":"Masud Alam","doi":"10.1007/s00181-024-02591-2","DOIUrl":null,"url":null,"abstract":"<p>This paper examines the short- and medium-run effects of U.S. federal personal income and corporate income tax cuts on a wide array of economic policy variables in a data-rich environment. Using a panel of U.S. macroeconomic data set, made up of 132 quarterly macroeconomic series for 1959–2018, we estimate factor-augmented vector autoregression (FAVARs) models where an extended narrative tax changes dataset combined with unobserved factors. The narrative approach classifies if tax changes are exogenous or endogenous. This paper identifies narrative tax shocks in the vector autoregression model using the sign restrictions with the Uhlig's (J Monet Econ 52(2):381–419, 2005. https://doi.org/10.1016/j.jmoneco.2004.05.007) penalty function. Empirical findings show a significant expansionary effect of tax cuts on the macroeconomic variables. Cuts in personal and corporate income taxes cause a rise in output, investment, employment, and consumption; however, the effects of corporate tax cuts have relatively smaller effects on output and consumption but show immediate and higher effects on fixed investment and price levels. We validate the model's specification and the identification of tax shocks through a reliability test based on the Median-Target method. Additionally, sensitivity analysis employing the local projection vector autoregression model, number of iterations of the algorithm, and incorporating diverse factor specifications reaffirms tax cuts' persistent and expansionary effects. Our contribution to the narrative tax literature lies in providing empirical evidence that aligns with the notion that reductions in personal taxes demonstrate a higher efficacy as a fiscal policy tool when compared to reductions in corporate income taxes.</p>","PeriodicalId":11642,"journal":{"name":"Empirical Economics","volume":"102 1","pages":""},"PeriodicalIF":1.9000,"publicationDate":"2024-04-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Output, employment, and price effects of U.S. narrative tax changes: a factor-augmented vector autoregression approach\",\"authors\":\"Masud Alam\",\"doi\":\"10.1007/s00181-024-02591-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper examines the short- and medium-run effects of U.S. federal personal income and corporate income tax cuts on a wide array of economic policy variables in a data-rich environment. Using a panel of U.S. macroeconomic data set, made up of 132 quarterly macroeconomic series for 1959–2018, we estimate factor-augmented vector autoregression (FAVARs) models where an extended narrative tax changes dataset combined with unobserved factors. The narrative approach classifies if tax changes are exogenous or endogenous. This paper identifies narrative tax shocks in the vector autoregression model using the sign restrictions with the Uhlig's (J Monet Econ 52(2):381–419, 2005. https://doi.org/10.1016/j.jmoneco.2004.05.007) penalty function. Empirical findings show a significant expansionary effect of tax cuts on the macroeconomic variables. Cuts in personal and corporate income taxes cause a rise in output, investment, employment, and consumption; however, the effects of corporate tax cuts have relatively smaller effects on output and consumption but show immediate and higher effects on fixed investment and price levels. We validate the model's specification and the identification of tax shocks through a reliability test based on the Median-Target method. Additionally, sensitivity analysis employing the local projection vector autoregression model, number of iterations of the algorithm, and incorporating diverse factor specifications reaffirms tax cuts' persistent and expansionary effects. Our contribution to the narrative tax literature lies in providing empirical evidence that aligns with the notion that reductions in personal taxes demonstrate a higher efficacy as a fiscal policy tool when compared to reductions in corporate income taxes.</p>\",\"PeriodicalId\":11642,\"journal\":{\"name\":\"Empirical Economics\",\"volume\":\"102 1\",\"pages\":\"\"},\"PeriodicalIF\":1.9000,\"publicationDate\":\"2024-04-17\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Empirical Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s00181-024-02591-2\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Empirical Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s00181-024-02591-2","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Output, employment, and price effects of U.S. narrative tax changes: a factor-augmented vector autoregression approach

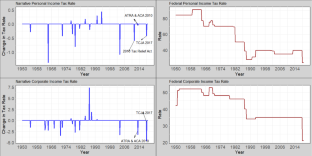

This paper examines the short- and medium-run effects of U.S. federal personal income and corporate income tax cuts on a wide array of economic policy variables in a data-rich environment. Using a panel of U.S. macroeconomic data set, made up of 132 quarterly macroeconomic series for 1959–2018, we estimate factor-augmented vector autoregression (FAVARs) models where an extended narrative tax changes dataset combined with unobserved factors. The narrative approach classifies if tax changes are exogenous or endogenous. This paper identifies narrative tax shocks in the vector autoregression model using the sign restrictions with the Uhlig's (J Monet Econ 52(2):381–419, 2005. https://doi.org/10.1016/j.jmoneco.2004.05.007) penalty function. Empirical findings show a significant expansionary effect of tax cuts on the macroeconomic variables. Cuts in personal and corporate income taxes cause a rise in output, investment, employment, and consumption; however, the effects of corporate tax cuts have relatively smaller effects on output and consumption but show immediate and higher effects on fixed investment and price levels. We validate the model's specification and the identification of tax shocks through a reliability test based on the Median-Target method. Additionally, sensitivity analysis employing the local projection vector autoregression model, number of iterations of the algorithm, and incorporating diverse factor specifications reaffirms tax cuts' persistent and expansionary effects. Our contribution to the narrative tax literature lies in providing empirical evidence that aligns with the notion that reductions in personal taxes demonstrate a higher efficacy as a fiscal policy tool when compared to reductions in corporate income taxes.

期刊介绍:

Empirical Economics publishes high quality papers using econometric or statistical methods to fill the gap between economic theory and observed data. Papers explore such topics as estimation of established relationships between economic variables, testing of hypotheses derived from economic theory, treatment effect estimation, policy evaluation, simulation, forecasting, as well as econometric methods and measurement. Empirical Economics emphasizes the replicability of empirical results. Replication studies of important results in the literature - both positive and negative results - may be published as short papers in Empirical Economics. Authors of all accepted papers and replications are required to submit all data and codes prior to publication (for more details, see: Instructions for Authors).The journal follows a single blind review procedure. In order to ensure the high quality of the journal and an efficient editorial process, a substantial number of submissions that have very poor chances of receiving positive reviews are routinely rejected without sending the papers for review.Officially cited as: Empir Econ

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们