{"title":"欧洲央行加息对匈牙利银行间同业拆借利率和欧元/匈牙利福林汇率有溢出效应吗?使用 Diebold-Yilmaz 溢出表的五变量 VAR 模型方法","authors":"Molnar Albert, Csiszárik-Kocsír Ágnes","doi":"10.1002/jcaf.22716","DOIUrl":null,"url":null,"abstract":"<p>We intend to show the directional volatility spillovers between the European short term interbank lending rates (3-month Euro Interbank Offered Rate [EURIBOR] and Euro Short-Term Rate [ESTR]) and the Hungarian Budapest Interbank Offered Rate (BUBOR) and Euro-Hungarian Forint exchange rate. To determine the extent to which the variables affect each other's volatilities we build a five-variable vector autoregression (VAR) and determine the spillover table like in Diebold-Yilmaz's 2012 work. This methodology is preferred to a simple impulse response function (IRF) because we manage to avoid the problem of non-orthogonal innovations via the generalized forecast error variance decomposition framework. The issue of variable ordering, therefore, does not arise. We focus on three episodes of increased volatility in Hungarian and European short-term interest rates: Q3–Q4 of 2019, Q1 of 2020 and Q3 of 2022. These episodes correspond to volatility spikes in EU markets that to some extent had a measurable spillover effect on Hungarian interbank rates. We find that on average, across the entire sample of 957 observations, about 6.3% of the volatility forecast error variance in all five European and Hungarian variables comes from spillovers. The total and directional spillovers over the sample are extremely low. We conclude that the European Central Bank's surprise policy decisions have a marginal impact on Hungarian interbank rates. We also find that BUBOR is primarily a net receiver of spillovers from the MAX short-term government bond benchmark rather than the EURIBOR—this disproved our initial considerations.</p>","PeriodicalId":44561,"journal":{"name":"Journal of Corporate Accounting and Finance","volume":"35 4","pages":"39-57"},"PeriodicalIF":0.9000,"publicationDate":"2024-04-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jcaf.22716","citationCount":"0","resultStr":"{\"title\":\"Do ECB's rate hikes have spillover effects on the Hungarian BUBOR and the EUR/HUF exchange rate? A five-variable VAR model approach using the Diebold-Yilmaz spillover table\",\"authors\":\"Molnar Albert, Csiszárik-Kocsír Ágnes\",\"doi\":\"10.1002/jcaf.22716\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We intend to show the directional volatility spillovers between the European short term interbank lending rates (3-month Euro Interbank Offered Rate [EURIBOR] and Euro Short-Term Rate [ESTR]) and the Hungarian Budapest Interbank Offered Rate (BUBOR) and Euro-Hungarian Forint exchange rate. To determine the extent to which the variables affect each other's volatilities we build a five-variable vector autoregression (VAR) and determine the spillover table like in Diebold-Yilmaz's 2012 work. This methodology is preferred to a simple impulse response function (IRF) because we manage to avoid the problem of non-orthogonal innovations via the generalized forecast error variance decomposition framework. The issue of variable ordering, therefore, does not arise. We focus on three episodes of increased volatility in Hungarian and European short-term interest rates: Q3–Q4 of 2019, Q1 of 2020 and Q3 of 2022. These episodes correspond to volatility spikes in EU markets that to some extent had a measurable spillover effect on Hungarian interbank rates. We find that on average, across the entire sample of 957 observations, about 6.3% of the volatility forecast error variance in all five European and Hungarian variables comes from spillovers. The total and directional spillovers over the sample are extremely low. We conclude that the European Central Bank's surprise policy decisions have a marginal impact on Hungarian interbank rates. We also find that BUBOR is primarily a net receiver of spillovers from the MAX short-term government bond benchmark rather than the EURIBOR—this disproved our initial considerations.</p>\",\"PeriodicalId\":44561,\"journal\":{\"name\":\"Journal of Corporate Accounting and Finance\",\"volume\":\"35 4\",\"pages\":\"39-57\"},\"PeriodicalIF\":0.9000,\"publicationDate\":\"2024-04-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jcaf.22716\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Corporate Accounting and Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/jcaf.22716\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Corporate Accounting and Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/jcaf.22716","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Do ECB's rate hikes have spillover effects on the Hungarian BUBOR and the EUR/HUF exchange rate? A five-variable VAR model approach using the Diebold-Yilmaz spillover table

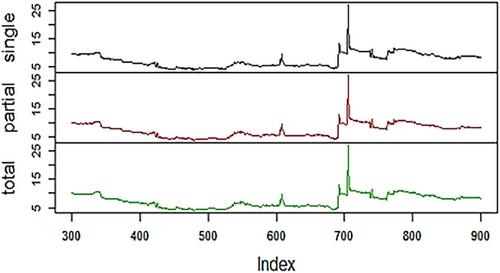

We intend to show the directional volatility spillovers between the European short term interbank lending rates (3-month Euro Interbank Offered Rate [EURIBOR] and Euro Short-Term Rate [ESTR]) and the Hungarian Budapest Interbank Offered Rate (BUBOR) and Euro-Hungarian Forint exchange rate. To determine the extent to which the variables affect each other's volatilities we build a five-variable vector autoregression (VAR) and determine the spillover table like in Diebold-Yilmaz's 2012 work. This methodology is preferred to a simple impulse response function (IRF) because we manage to avoid the problem of non-orthogonal innovations via the generalized forecast error variance decomposition framework. The issue of variable ordering, therefore, does not arise. We focus on three episodes of increased volatility in Hungarian and European short-term interest rates: Q3–Q4 of 2019, Q1 of 2020 and Q3 of 2022. These episodes correspond to volatility spikes in EU markets that to some extent had a measurable spillover effect on Hungarian interbank rates. We find that on average, across the entire sample of 957 observations, about 6.3% of the volatility forecast error variance in all five European and Hungarian variables comes from spillovers. The total and directional spillovers over the sample are extremely low. We conclude that the European Central Bank's surprise policy decisions have a marginal impact on Hungarian interbank rates. We also find that BUBOR is primarily a net receiver of spillovers from the MAX short-term government bond benchmark rather than the EURIBOR—this disproved our initial considerations.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们