{"title":"美国与能源相关的不确定性冲击和通胀动态:一种多元量值回归方法","authors":"Ojonugwa Usman , Oktay Ozkan , Ayben Koy , Tomiwa Sunday Adebayo","doi":"10.1016/j.strueco.2024.07.012","DOIUrl":null,"url":null,"abstract":"<div><p>Existing literature suggests that uncertainty shocks can propagate like aggregate demand shocks or aggregate supply shocks. By way of extension, this study investigates the effect of energy-related uncertainty shocks on U.S. inflation while incorporating the effect of industrial production and interest rate uncertainty shocks. Using a multivariate quantile-on-quantile regression for the period 2000:M6 to 2019:M7, the findings reveal that energy-related uncertainty shocks amplify inflation by manifesting as cost-push shocks with a stronger connection emerging in quantiles slightly above the median quantile distribution of energy-related uncertainty. Although industrial production positively drives inflation, its effect is observed less around median quantiles of inflation than in the lower and upper quantiles. Furthermore, the effect of interest rate uncertainty is negative and stronger in quantiles around the median of inflation, suggesting that interest rate uncertainty behaves like aggregate demand shocks. Based on these findings, policy implications are offered.</p></div>","PeriodicalId":47829,"journal":{"name":"Structural Change and Economic Dynamics","volume":"71 ","pages":""},"PeriodicalIF":5.5000,"publicationDate":"2024-12-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Energy-related uncertainty shocks and inflation dynamics in the U.S: A multivariate quantile-on-quantile regression approach\",\"authors\":\"Ojonugwa Usman , Oktay Ozkan , Ayben Koy , Tomiwa Sunday Adebayo\",\"doi\":\"10.1016/j.strueco.2024.07.012\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>Existing literature suggests that uncertainty shocks can propagate like aggregate demand shocks or aggregate supply shocks. By way of extension, this study investigates the effect of energy-related uncertainty shocks on U.S. inflation while incorporating the effect of industrial production and interest rate uncertainty shocks. Using a multivariate quantile-on-quantile regression for the period 2000:M6 to 2019:M7, the findings reveal that energy-related uncertainty shocks amplify inflation by manifesting as cost-push shocks with a stronger connection emerging in quantiles slightly above the median quantile distribution of energy-related uncertainty. Although industrial production positively drives inflation, its effect is observed less around median quantiles of inflation than in the lower and upper quantiles. Furthermore, the effect of interest rate uncertainty is negative and stronger in quantiles around the median of inflation, suggesting that interest rate uncertainty behaves like aggregate demand shocks. Based on these findings, policy implications are offered.</p></div>\",\"PeriodicalId\":47829,\"journal\":{\"name\":\"Structural Change and Economic Dynamics\",\"volume\":\"71 \",\"pages\":\"\"},\"PeriodicalIF\":5.5000,\"publicationDate\":\"2024-12-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Structural Change and Economic Dynamics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://www.sciencedirect.com/science/article/pii/S0954349X24001073\",\"RegionNum\":2,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2024/7/31 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"Q1\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Structural Change and Economic Dynamics","FirstCategoryId":"96","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S0954349X24001073","RegionNum":2,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2024/7/31 0:00:00","PubModel":"Epub","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

Energy-related uncertainty shocks and inflation dynamics in the U.S: A multivariate quantile-on-quantile regression approach

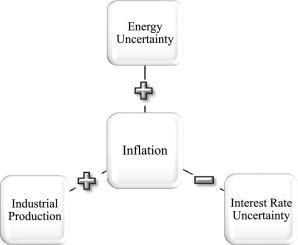

Existing literature suggests that uncertainty shocks can propagate like aggregate demand shocks or aggregate supply shocks. By way of extension, this study investigates the effect of energy-related uncertainty shocks on U.S. inflation while incorporating the effect of industrial production and interest rate uncertainty shocks. Using a multivariate quantile-on-quantile regression for the period 2000:M6 to 2019:M7, the findings reveal that energy-related uncertainty shocks amplify inflation by manifesting as cost-push shocks with a stronger connection emerging in quantiles slightly above the median quantile distribution of energy-related uncertainty. Although industrial production positively drives inflation, its effect is observed less around median quantiles of inflation than in the lower and upper quantiles. Furthermore, the effect of interest rate uncertainty is negative and stronger in quantiles around the median of inflation, suggesting that interest rate uncertainty behaves like aggregate demand shocks. Based on these findings, policy implications are offered.

期刊介绍:

Structural Change and Economic Dynamics publishes articles about theoretical, applied and methodological aspects of structural change in economic systems. The journal publishes work analysing dynamics and structural breaks in economic, technological, behavioural and institutional patterns.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们