{"title":"遵守还是解释?企业在强制性环境信息披露计划中是否伺机索取商业秘密?","authors":"YILE (ANSON) JIANG","doi":"10.1111/1475-679X.12583","DOIUrl":null,"url":null,"abstract":"<p>This paper studies whether firms opportunistically make proprietary claims in mandatory environmental disclosure programs with trade secret exemption rules. Examining the mandatory chemical disclosure program in the fracking industry, I find evidence of opportunistic withholding of information among operators that are less likely to have trade secrets. Specifically, I find that these operators claim fewer chemicals as trade secrets when the operating site is in close proximity to water quality monitors. This is only observed among publicly traded operators that face a higher cost of societal backlash when disclosing pollutant information. Further analyses suggest that these operators are concerned about external environmental monitoring, which deters them from opportunistic information withholding. Regarding public and private operators that are more likely to have trade secrets, I do not find strong evidence that their information withholding varies with the monitoring conditions.</p>","PeriodicalId":48414,"journal":{"name":"Journal of Accounting Research","volume":"62 5","pages":"1755-1794"},"PeriodicalIF":6.3000,"publicationDate":"2024-10-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-679X.12583","citationCount":"0","resultStr":"{\"title\":\"Comply or Explain: Do Firms Opportunistically Claim Trade Secrets in Mandatory Environmental Disclosure Programs?\",\"authors\":\"YILE (ANSON) JIANG\",\"doi\":\"10.1111/1475-679X.12583\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper studies whether firms opportunistically make proprietary claims in mandatory environmental disclosure programs with trade secret exemption rules. Examining the mandatory chemical disclosure program in the fracking industry, I find evidence of opportunistic withholding of information among operators that are less likely to have trade secrets. Specifically, I find that these operators claim fewer chemicals as trade secrets when the operating site is in close proximity to water quality monitors. This is only observed among publicly traded operators that face a higher cost of societal backlash when disclosing pollutant information. Further analyses suggest that these operators are concerned about external environmental monitoring, which deters them from opportunistic information withholding. Regarding public and private operators that are more likely to have trade secrets, I do not find strong evidence that their information withholding varies with the monitoring conditions.</p>\",\"PeriodicalId\":48414,\"journal\":{\"name\":\"Journal of Accounting Research\",\"volume\":\"62 5\",\"pages\":\"1755-1794\"},\"PeriodicalIF\":6.3000,\"publicationDate\":\"2024-10-15\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-679X.12583\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.12583\",\"RegionNum\":2,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.12583","RegionNum":2,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Comply or Explain: Do Firms Opportunistically Claim Trade Secrets in Mandatory Environmental Disclosure Programs?

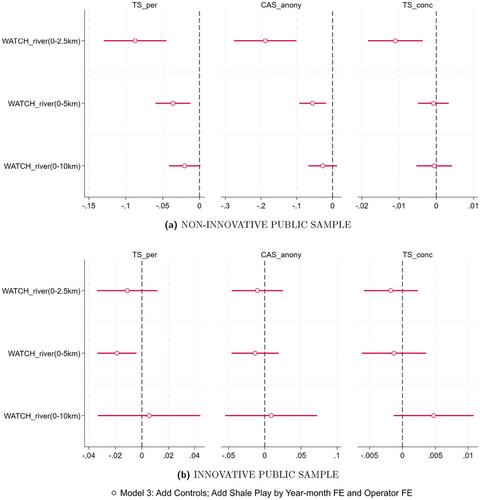

This paper studies whether firms opportunistically make proprietary claims in mandatory environmental disclosure programs with trade secret exemption rules. Examining the mandatory chemical disclosure program in the fracking industry, I find evidence of opportunistic withholding of information among operators that are less likely to have trade secrets. Specifically, I find that these operators claim fewer chemicals as trade secrets when the operating site is in close proximity to water quality monitors. This is only observed among publicly traded operators that face a higher cost of societal backlash when disclosing pollutant information. Further analyses suggest that these operators are concerned about external environmental monitoring, which deters them from opportunistic information withholding. Regarding public and private operators that are more likely to have trade secrets, I do not find strong evidence that their information withholding varies with the monitoring conditions.

期刊介绍:

The Journal of Accounting Research is a general-interest accounting journal. It publishes original research in all areas of accounting and related fields that utilizes tools from basic disciplines such as economics, statistics, psychology, and sociology. This research typically uses analytical, empirical archival, experimental, and field study methods and addresses economic questions, external and internal, in accounting, auditing, disclosure, financial reporting, taxation, and information as well as related fields such as corporate finance, investments, capital markets, law, contracting, and information economics.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们