{"title":"测量误差模型控制图","authors":"Vasyl Golosnoy, Benno Hildebrandt, Steffen Köhler, Wolfgang Schmid, Miriam Isabel Seifert","doi":"10.1007/s10182-022-00462-8","DOIUrl":null,"url":null,"abstract":"<div><p>We consider a linear measurement error model (MEM) with AR(1) process in the state equation which is widely used in applied research. This MEM could be equivalently re-written as ARMA(1,1) process, where the MA(1) parameter is related to the variance of measurement errors. As the MA(1) parameter is of essential importance for these linear MEMs, it is of much relevance to provide instruments for online monitoring in order to detect its possible changes. In this paper we develop control charts for online detection of such changes, i.e., from AR(1) to ARMA(1,1) and vice versa, as soon as they occur. For this purpose, we elaborate on both cumulative sum (CUSUM) and exponentially weighted moving average (EWMA) control charts and investigate their performance in a Monte Carlo simulation study. The empirical illustration of our approach is conducted based on time series of daily realized volatilities.\n</p></div>","PeriodicalId":55446,"journal":{"name":"Asta-Advances in Statistical Analysis","volume":"107 4","pages":"693 - 712"},"PeriodicalIF":1.4000,"publicationDate":"2022-10-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9533293/pdf/","citationCount":"0","resultStr":"{\"title\":\"Control charts for measurement error models\",\"authors\":\"Vasyl Golosnoy, Benno Hildebrandt, Steffen Köhler, Wolfgang Schmid, Miriam Isabel Seifert\",\"doi\":\"10.1007/s10182-022-00462-8\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>We consider a linear measurement error model (MEM) with AR(1) process in the state equation which is widely used in applied research. This MEM could be equivalently re-written as ARMA(1,1) process, where the MA(1) parameter is related to the variance of measurement errors. As the MA(1) parameter is of essential importance for these linear MEMs, it is of much relevance to provide instruments for online monitoring in order to detect its possible changes. In this paper we develop control charts for online detection of such changes, i.e., from AR(1) to ARMA(1,1) and vice versa, as soon as they occur. For this purpose, we elaborate on both cumulative sum (CUSUM) and exponentially weighted moving average (EWMA) control charts and investigate their performance in a Monte Carlo simulation study. The empirical illustration of our approach is conducted based on time series of daily realized volatilities.\\n</p></div>\",\"PeriodicalId\":55446,\"journal\":{\"name\":\"Asta-Advances in Statistical Analysis\",\"volume\":\"107 4\",\"pages\":\"693 - 712\"},\"PeriodicalIF\":1.4000,\"publicationDate\":\"2022-10-05\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9533293/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asta-Advances in Statistical Analysis\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10182-022-00462-8\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asta-Advances in Statistical Analysis","FirstCategoryId":"100","ListUrlMain":"https://link.springer.com/article/10.1007/s10182-022-00462-8","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

引用次数: 0

摘要

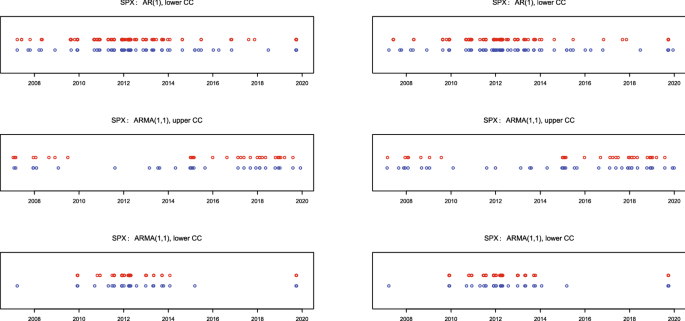

我们考虑的是状态方程中含有 AR(1) 过程的线性测量误差模型 (MEM),该模型在应用研究中被广泛使用。这种 MEM 可以等价地改写为 ARMA(1,1) 过程,其中 MA(1) 参数与测量误差的方差有关。由于 MA(1) 参数对这些线性 MEM 至关重要,因此提供在线监测仪器以检测其可能的变化具有重要意义。在本文中,我们开发了在线检测这种变化的控制图,即从 AR(1) 到 ARMA(1,1) 以及反之亦然。为此,我们详细阐述了累积和(CUSUM)和指数加权移动平均(EWMA)控制图,并在蒙特卡罗模拟研究中调查了它们的性能。我们根据每日已实现波动率的时间序列对我们的方法进行了实证说明。

We consider a linear measurement error model (MEM) with AR(1) process in the state equation which is widely used in applied research. This MEM could be equivalently re-written as ARMA(1,1) process, where the MA(1) parameter is related to the variance of measurement errors. As the MA(1) parameter is of essential importance for these linear MEMs, it is of much relevance to provide instruments for online monitoring in order to detect its possible changes. In this paper we develop control charts for online detection of such changes, i.e., from AR(1) to ARMA(1,1) and vice versa, as soon as they occur. For this purpose, we elaborate on both cumulative sum (CUSUM) and exponentially weighted moving average (EWMA) control charts and investigate their performance in a Monte Carlo simulation study. The empirical illustration of our approach is conducted based on time series of daily realized volatilities.

期刊介绍:

AStA - Advances in Statistical Analysis, a journal of the German Statistical Society, is published quarterly and presents original contributions on statistical methods and applications and review articles.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们