{"title":"西班牙增税的宏观经济和分配效应。","authors":"Luisa Fuster","doi":"10.1007/s13209-022-00269-5","DOIUrl":null,"url":null,"abstract":"<p><p>I assess the macroeconomic and redistributive effects of tax reforms aimed at increasing tax revenue in Spain. To this end, I develop a theory of entrepreneurship that mimics key facts on the wealth and income distribution in Spain. I find two reforms that raise fiscal pressure in Spain to the average value among countries in the Euro area. The first reform involves doubling the average effective tax rate on labor and business income for all individuals whose income is above a threshold level. I find that this reform reduces the inequality in after-tax income, wealth, and consumption. However, it implies a substantial GDP reduction. The second reform increases the flat tax rate on consumption by fifteen percentage points. While this reform does not reduce long-run output, it does not decrease household inequality. All in all, the desirability of the two reforms depends on the government's preferences for reducing inequality at the expense of aggregate output losses.</p>","PeriodicalId":54185,"journal":{"name":"Series-Journal of the Spanish Economic Association","volume":"13 4","pages":"613-648"},"PeriodicalIF":0.5000,"publicationDate":"2022-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9643962/pdf/","citationCount":"0","resultStr":"{\"title\":\"Macroeconomic and distributive effects of increasing taxes in Spain.\",\"authors\":\"Luisa Fuster\",\"doi\":\"10.1007/s13209-022-00269-5\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>I assess the macroeconomic and redistributive effects of tax reforms aimed at increasing tax revenue in Spain. To this end, I develop a theory of entrepreneurship that mimics key facts on the wealth and income distribution in Spain. I find two reforms that raise fiscal pressure in Spain to the average value among countries in the Euro area. The first reform involves doubling the average effective tax rate on labor and business income for all individuals whose income is above a threshold level. I find that this reform reduces the inequality in after-tax income, wealth, and consumption. However, it implies a substantial GDP reduction. The second reform increases the flat tax rate on consumption by fifteen percentage points. While this reform does not reduce long-run output, it does not decrease household inequality. All in all, the desirability of the two reforms depends on the government's preferences for reducing inequality at the expense of aggregate output losses.</p>\",\"PeriodicalId\":54185,\"journal\":{\"name\":\"Series-Journal of the Spanish Economic Association\",\"volume\":\"13 4\",\"pages\":\"613-648\"},\"PeriodicalIF\":0.5000,\"publicationDate\":\"2022-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9643962/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Series-Journal of the Spanish Economic Association\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s13209-022-00269-5\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2022/11/9 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Series-Journal of the Spanish Economic Association","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s13209-022-00269-5","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2022/11/9 0:00:00","PubModel":"Epub","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Macroeconomic and distributive effects of increasing taxes in Spain.

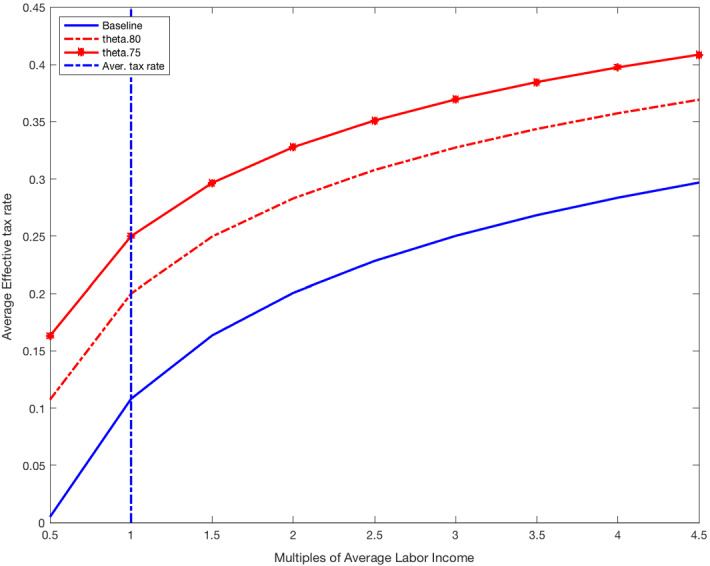

I assess the macroeconomic and redistributive effects of tax reforms aimed at increasing tax revenue in Spain. To this end, I develop a theory of entrepreneurship that mimics key facts on the wealth and income distribution in Spain. I find two reforms that raise fiscal pressure in Spain to the average value among countries in the Euro area. The first reform involves doubling the average effective tax rate on labor and business income for all individuals whose income is above a threshold level. I find that this reform reduces the inequality in after-tax income, wealth, and consumption. However, it implies a substantial GDP reduction. The second reform increases the flat tax rate on consumption by fifteen percentage points. While this reform does not reduce long-run output, it does not decrease household inequality. All in all, the desirability of the two reforms depends on the government's preferences for reducing inequality at the expense of aggregate output losses.

期刊介绍:

SERIEs is a single-blind peer-reviewed open access journal. In the Journal Citation Reports (JCR) the impact factor of the journal in 2020 is 1.088 and, in Scopus, we are in the top quartile according to Scimago Journal Ranking and the CiteScores.

SERIEs - Journal of the Spanish Economic Association is the result of a merger between the two most important academic economics journals in Spain: Spanish Economic Review (SER) and Investigaciones Económicas (IE). The new journal publishes scientific articles in all areas of economics. We welcome both theoretical and empirical papers and place great value on applying high quality standards.

SERIEs seeks to maintain the reputation gained by its predecessors as the most prominent economics journals in Spain, and to become a major internationally recognized journal. The journal is receptive to high-quality papers on any topic and from any source. At the same time, as official journal of the Spanish Economic Association, SERIEs is very interested in high-quality empirical papers about the Spanish and the European economy.

The publication costs are covered by Spanish Economic Association so authors do not need to pay an article-processing charge.

The journal operates a single-blind peer-review system, where the reviewers are aware of the names and affiliations of the authors, but the reviewer reports provided to authors are anonymous.

SERIEs encourages authors to share their data where possible. For further details on the data policy for the journal please see the Springer Nature page here: https://www.springernature.com/gp/authors/research-data-policy/repositories-general/12327166

Officially cited as: SERIEs-Journal of the Spanish Economic Association

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们