{"title":"可预测的正向性能过程:人机交互的罕见评估和应用","authors":"Gechun Liang, Moris S. Strub, Yuwei Wang","doi":"10.1111/mafi.12408","DOIUrl":null,"url":null,"abstract":"<p>We study discrete-time predictable forward processes when trading times do not coincide with performance evaluation times in a binomial tree model for the financial market. The key step in the construction of these processes is to solve a linear functional equation of higher order associated with the inverse problem driving the evolution of the predictable forward process. We provide sufficient conditions for the existence and uniqueness and an explicit construction of the predictable forward process under these conditions. Furthermore, we find that these processes are inherently myopic in the sense that optimal strategies do not make use of future model parameters even if these are known. Finally, we argue that predictable forward preferences are a viable framework to model human-machine interactions occurring in automated trading or robo-advising. For both applications, we determine an optimal interaction schedule of a human agent interacting infrequently with a machine that is in charge of trading.</p>","PeriodicalId":49867,"journal":{"name":"Mathematical Finance","volume":"33 4","pages":"1248-1286"},"PeriodicalIF":2.4000,"publicationDate":"2023-07-02","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/mafi.12408","citationCount":"2","resultStr":"{\"title\":\"Predictable forward performance processes: Infrequent evaluation and applications to human-machine interactions\",\"authors\":\"Gechun Liang, Moris S. Strub, Yuwei Wang\",\"doi\":\"10.1111/mafi.12408\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We study discrete-time predictable forward processes when trading times do not coincide with performance evaluation times in a binomial tree model for the financial market. The key step in the construction of these processes is to solve a linear functional equation of higher order associated with the inverse problem driving the evolution of the predictable forward process. We provide sufficient conditions for the existence and uniqueness and an explicit construction of the predictable forward process under these conditions. Furthermore, we find that these processes are inherently myopic in the sense that optimal strategies do not make use of future model parameters even if these are known. Finally, we argue that predictable forward preferences are a viable framework to model human-machine interactions occurring in automated trading or robo-advising. For both applications, we determine an optimal interaction schedule of a human agent interacting infrequently with a machine that is in charge of trading.</p>\",\"PeriodicalId\":49867,\"journal\":{\"name\":\"Mathematical Finance\",\"volume\":\"33 4\",\"pages\":\"1248-1286\"},\"PeriodicalIF\":2.4000,\"publicationDate\":\"2023-07-02\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/mafi.12408\",\"citationCount\":\"2\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Mathematical Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/mafi.12408\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Mathematical Finance","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/mafi.12408","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Predictable forward performance processes: Infrequent evaluation and applications to human-machine interactions

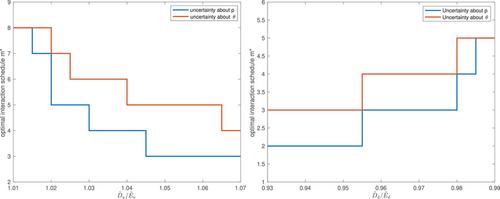

We study discrete-time predictable forward processes when trading times do not coincide with performance evaluation times in a binomial tree model for the financial market. The key step in the construction of these processes is to solve a linear functional equation of higher order associated with the inverse problem driving the evolution of the predictable forward process. We provide sufficient conditions for the existence and uniqueness and an explicit construction of the predictable forward process under these conditions. Furthermore, we find that these processes are inherently myopic in the sense that optimal strategies do not make use of future model parameters even if these are known. Finally, we argue that predictable forward preferences are a viable framework to model human-machine interactions occurring in automated trading or robo-advising. For both applications, we determine an optimal interaction schedule of a human agent interacting infrequently with a machine that is in charge of trading.

期刊介绍:

Mathematical Finance seeks to publish original research articles focused on the development and application of novel mathematical and statistical methods for the analysis of financial problems.

The journal welcomes contributions on new statistical methods for the analysis of financial problems. Empirical results will be appropriate to the extent that they illustrate a statistical technique, validate a model or provide insight into a financial problem. Papers whose main contribution rests on empirical results derived with standard approaches will not be considered.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们