Stewart Jones, William J. Moser, Matthew M. Wieland

{"title":"机器学习和盈利能力变化的预测","authors":"Stewart Jones, William J. Moser, Matthew M. Wieland","doi":"10.1111/1911-3846.12888","DOIUrl":null,"url":null,"abstract":"<p>This study uses machine-learning methods to predict next-period change in profitability based on a model proposed by Penman and Zhang (2004, Working paper, Columbia University and University of California, Berkeley; “PZ”). We find that new machine-learning methods predict out of sample substantially better than traditional regression methods and provide richer interpretations about the role and impact of different predictor variables through their nonlinear relationships and interaction effects. For example, our results contrast with previous research by showing that both components of the DuPont decomposition (change in profit margin and change in asset turnover) are informative of next-period changes in profitability. Our results are robust across different performance metrics, alternative machine-learning models, and software. Furthermore, an unconstrained machine-learning model using a larger feature space could not significantly improve the performance of the PZ model. PZ variables alone accounted for most of the explanatory power of the unconstrained model, suggesting the PZ model is both well specified (in terms of feature selection) and robust in higher dimensional settings. With respect to the economic significance of this information, we find mixed results. The market appears to adjust its expectations more in line with the machine-learning predictions relative to the PZ model but the portfolio returns are not significantly different.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"40 4","pages":"2643-2672"},"PeriodicalIF":3.8000,"publicationDate":"2023-07-10","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12888","citationCount":"0","resultStr":"{\"title\":\"Machine learning and the prediction of changes in profitability\",\"authors\":\"Stewart Jones, William J. Moser, Matthew M. Wieland\",\"doi\":\"10.1111/1911-3846.12888\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This study uses machine-learning methods to predict next-period change in profitability based on a model proposed by Penman and Zhang (2004, Working paper, Columbia University and University of California, Berkeley; “PZ”). We find that new machine-learning methods predict out of sample substantially better than traditional regression methods and provide richer interpretations about the role and impact of different predictor variables through their nonlinear relationships and interaction effects. For example, our results contrast with previous research by showing that both components of the DuPont decomposition (change in profit margin and change in asset turnover) are informative of next-period changes in profitability. Our results are robust across different performance metrics, alternative machine-learning models, and software. Furthermore, an unconstrained machine-learning model using a larger feature space could not significantly improve the performance of the PZ model. PZ variables alone accounted for most of the explanatory power of the unconstrained model, suggesting the PZ model is both well specified (in terms of feature selection) and robust in higher dimensional settings. With respect to the economic significance of this information, we find mixed results. The market appears to adjust its expectations more in line with the machine-learning predictions relative to the PZ model but the portfolio returns are not significantly different.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"40 4\",\"pages\":\"2643-2672\"},\"PeriodicalIF\":3.8000,\"publicationDate\":\"2023-07-10\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12888\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12888\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12888","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Machine learning and the prediction of changes in profitability

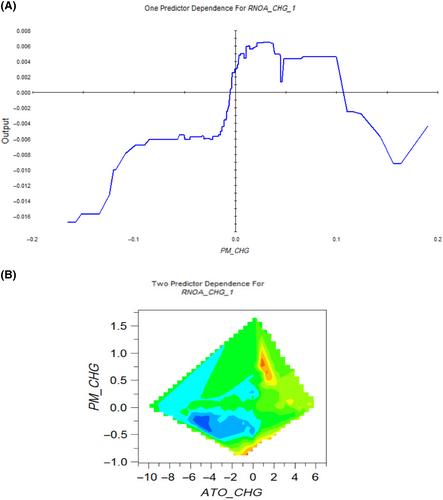

This study uses machine-learning methods to predict next-period change in profitability based on a model proposed by Penman and Zhang (2004, Working paper, Columbia University and University of California, Berkeley; “PZ”). We find that new machine-learning methods predict out of sample substantially better than traditional regression methods and provide richer interpretations about the role and impact of different predictor variables through their nonlinear relationships and interaction effects. For example, our results contrast with previous research by showing that both components of the DuPont decomposition (change in profit margin and change in asset turnover) are informative of next-period changes in profitability. Our results are robust across different performance metrics, alternative machine-learning models, and software. Furthermore, an unconstrained machine-learning model using a larger feature space could not significantly improve the performance of the PZ model. PZ variables alone accounted for most of the explanatory power of the unconstrained model, suggesting the PZ model is both well specified (in terms of feature selection) and robust in higher dimensional settings. With respect to the economic significance of this information, we find mixed results. The market appears to adjust its expectations more in line with the machine-learning predictions relative to the PZ model but the portfolio returns are not significantly different.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们