{"title":"审计合作伙伴的识别、匹配和审计人才的劳动力市场","authors":"Mingcherng Deng, Eunhee Kim, Minlei Ye","doi":"10.1111/1911-3846.12878","DOIUrl":null,"url":null,"abstract":"<p>Conventional wisdom suggests that audit engagement partner name disclosure benefits investors by informing them about the partners' performance. However, such public disclosure of the identity of the audit partners may also intensify competition for audit talent in the labor market. To examine the economic consequences of audit partner identification, we build a two-period model in which an audit firm matches partners to clients. The audit partner identification broadens a partner's outside options in the labor market, making talent retention more costly. If the talent-retention cost is substantial, audit partner identification may cause an audit firm to adjust its partners' compensation packages and mismatch the partners and clients, which may lead to lower audit quality. Overall, we identify unintended consequences of audit partner identification by examining its impact on the audit labor market, and we provide economic reasons for the mixed empirical findings.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"40 3","pages":"2140-2163"},"PeriodicalIF":3.8000,"publicationDate":"2023-05-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12878","citationCount":"0","resultStr":"{\"title\":\"Audit partner identification, matching, and the labor market for audit talent\",\"authors\":\"Mingcherng Deng, Eunhee Kim, Minlei Ye\",\"doi\":\"10.1111/1911-3846.12878\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Conventional wisdom suggests that audit engagement partner name disclosure benefits investors by informing them about the partners' performance. However, such public disclosure of the identity of the audit partners may also intensify competition for audit talent in the labor market. To examine the economic consequences of audit partner identification, we build a two-period model in which an audit firm matches partners to clients. The audit partner identification broadens a partner's outside options in the labor market, making talent retention more costly. If the talent-retention cost is substantial, audit partner identification may cause an audit firm to adjust its partners' compensation packages and mismatch the partners and clients, which may lead to lower audit quality. Overall, we identify unintended consequences of audit partner identification by examining its impact on the audit labor market, and we provide economic reasons for the mixed empirical findings.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"40 3\",\"pages\":\"2140-2163\"},\"PeriodicalIF\":3.8000,\"publicationDate\":\"2023-05-31\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12878\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12878\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12878","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Audit partner identification, matching, and the labor market for audit talent

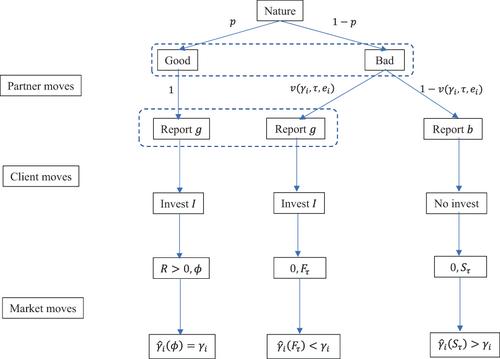

Conventional wisdom suggests that audit engagement partner name disclosure benefits investors by informing them about the partners' performance. However, such public disclosure of the identity of the audit partners may also intensify competition for audit talent in the labor market. To examine the economic consequences of audit partner identification, we build a two-period model in which an audit firm matches partners to clients. The audit partner identification broadens a partner's outside options in the labor market, making talent retention more costly. If the talent-retention cost is substantial, audit partner identification may cause an audit firm to adjust its partners' compensation packages and mismatch the partners and clients, which may lead to lower audit quality. Overall, we identify unintended consequences of audit partner identification by examining its impact on the audit labor market, and we provide economic reasons for the mixed empirical findings.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们