{"title":"第四次工业革命中的审计师判断","authors":"Rita Samiolo, Crawford Spence, Dorothy Toh","doi":"10.1111/1911-3846.12901","DOIUrl":null,"url":null,"abstract":"<p>Discourse proclaiming the advent of a fourth industrial revolution predicts significant disruption to various work domains in the near future. Auditing is one of the domains where bold claims about the potential of technology are being made, with technology expected to augment auditors' judgments and, in time, possibly automate them. Drawing on 44 in-depth interviews with auditors, regulators, and emergent artificial intelligence software providers, we question the prevailing narrative around technological change in auditing which suggests that ostensibly simple, low-level technical tasks are areas where little judgment is at play and thus are ripe for automation. We show that significant elements of deliberation, sensemaking, and reflexivity, arguably critical for the socialization of early career auditors into the profession, may be lost when automating areas of work perceived as low value, leading us to question what it means to apply judgment in auditing. Conversely, higher-level aspects of the audit process may be assisted by technology and augmented in different ways, yet new technological structures generate new areas of indeterminacy that pose new and yet unresolved demands on auditors' judgment. Overall, the paper shows how auditor habits are changing and highlights the risks posed by new technologies to the acquisition of practical knowledge by auditors.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"41 1","pages":"498-528"},"PeriodicalIF":3.8000,"publicationDate":"2023-08-25","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12901","citationCount":"0","resultStr":"{\"title\":\"Auditor judgment in the fourth industrial revolution\",\"authors\":\"Rita Samiolo, Crawford Spence, Dorothy Toh\",\"doi\":\"10.1111/1911-3846.12901\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Discourse proclaiming the advent of a fourth industrial revolution predicts significant disruption to various work domains in the near future. Auditing is one of the domains where bold claims about the potential of technology are being made, with technology expected to augment auditors' judgments and, in time, possibly automate them. Drawing on 44 in-depth interviews with auditors, regulators, and emergent artificial intelligence software providers, we question the prevailing narrative around technological change in auditing which suggests that ostensibly simple, low-level technical tasks are areas where little judgment is at play and thus are ripe for automation. We show that significant elements of deliberation, sensemaking, and reflexivity, arguably critical for the socialization of early career auditors into the profession, may be lost when automating areas of work perceived as low value, leading us to question what it means to apply judgment in auditing. Conversely, higher-level aspects of the audit process may be assisted by technology and augmented in different ways, yet new technological structures generate new areas of indeterminacy that pose new and yet unresolved demands on auditors' judgment. Overall, the paper shows how auditor habits are changing and highlights the risks posed by new technologies to the acquisition of practical knowledge by auditors.</p>\",\"PeriodicalId\":10595,\"journal\":{\"name\":\"Contemporary Accounting Research\",\"volume\":\"41 1\",\"pages\":\"498-528\"},\"PeriodicalIF\":3.8000,\"publicationDate\":\"2023-08-25\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12901\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Contemporary Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12901\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12901","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Auditor judgment in the fourth industrial revolution

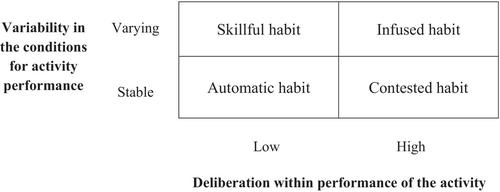

Discourse proclaiming the advent of a fourth industrial revolution predicts significant disruption to various work domains in the near future. Auditing is one of the domains where bold claims about the potential of technology are being made, with technology expected to augment auditors' judgments and, in time, possibly automate them. Drawing on 44 in-depth interviews with auditors, regulators, and emergent artificial intelligence software providers, we question the prevailing narrative around technological change in auditing which suggests that ostensibly simple, low-level technical tasks are areas where little judgment is at play and thus are ripe for automation. We show that significant elements of deliberation, sensemaking, and reflexivity, arguably critical for the socialization of early career auditors into the profession, may be lost when automating areas of work perceived as low value, leading us to question what it means to apply judgment in auditing. Conversely, higher-level aspects of the audit process may be assisted by technology and augmented in different ways, yet new technological structures generate new areas of indeterminacy that pose new and yet unresolved demands on auditors' judgment. Overall, the paper shows how auditor habits are changing and highlights the risks posed by new technologies to the acquisition of practical knowledge by auditors.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们