{"title":"政治/政策不确定性、公司信息披露与信息不对称","authors":"Lijun (Gillian) Lei, Yan Luo","doi":"10.1111/1911-3838.12317","DOIUrl":null,"url":null,"abstract":"<p>Political/policy uncertainty causes significant disruption to capital markets around the world. This review synthesizes recent studies on this topic and provides suggestions for future research in this fast-growing area. Specifically, this review focuses on three areas of research: (i) the measurement of political/policy uncertainty, (ii) the impact of political/policy uncertainty on financial analysts' forecasts, and (iii) the impact of political/policy uncertainty on corporate disclosure. We find that political/policy uncertainty affects both corporate disclosures and financial analysts' forecasts and that these effects interact with information asymmetry in capital markets. Furthermore, we find that companies strategically change their disclosure practices during periods of heightened political/policy uncertainty.</p>","PeriodicalId":43435,"journal":{"name":"Accounting Perspectives","volume":"22 1","pages":"87-110"},"PeriodicalIF":0.9000,"publicationDate":"2022-07-23","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3838.12317","citationCount":"2","resultStr":"{\"title\":\"Political/Policy Uncertainty, Corporate Disclosure, and Information Asymmetry*\",\"authors\":\"Lijun (Gillian) Lei, Yan Luo\",\"doi\":\"10.1111/1911-3838.12317\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Political/policy uncertainty causes significant disruption to capital markets around the world. This review synthesizes recent studies on this topic and provides suggestions for future research in this fast-growing area. Specifically, this review focuses on three areas of research: (i) the measurement of political/policy uncertainty, (ii) the impact of political/policy uncertainty on financial analysts' forecasts, and (iii) the impact of political/policy uncertainty on corporate disclosure. We find that political/policy uncertainty affects both corporate disclosures and financial analysts' forecasts and that these effects interact with information asymmetry in capital markets. Furthermore, we find that companies strategically change their disclosure practices during periods of heightened political/policy uncertainty.</p>\",\"PeriodicalId\":43435,\"journal\":{\"name\":\"Accounting Perspectives\",\"volume\":\"22 1\",\"pages\":\"87-110\"},\"PeriodicalIF\":0.9000,\"publicationDate\":\"2022-07-23\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3838.12317\",\"citationCount\":\"2\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Accounting Perspectives\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1911-3838.12317\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Accounting Perspectives","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3838.12317","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Political/Policy Uncertainty, Corporate Disclosure, and Information Asymmetry*

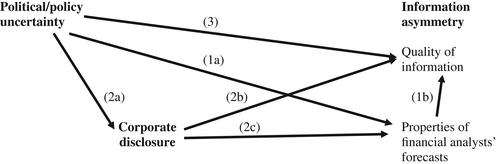

Political/policy uncertainty causes significant disruption to capital markets around the world. This review synthesizes recent studies on this topic and provides suggestions for future research in this fast-growing area. Specifically, this review focuses on three areas of research: (i) the measurement of political/policy uncertainty, (ii) the impact of political/policy uncertainty on financial analysts' forecasts, and (iii) the impact of political/policy uncertainty on corporate disclosure. We find that political/policy uncertainty affects both corporate disclosures and financial analysts' forecasts and that these effects interact with information asymmetry in capital markets. Furthermore, we find that companies strategically change their disclosure practices during periods of heightened political/policy uncertainty.

期刊介绍:

Accounting Perspectives provides a forum for peer-reviewed applied research, analysis, synthesis and commentary on issues of interest to academics, practitioners, financial analysts, financial executives, regulators, accounting policy makers and accounting students. Articles are sought from academics and practitioners that address relevant issues in any and all areas of accounting and related fields, including financial accounting and reporting, auditing and other assurance services, management accounting and performance measurement, information systems and related technologies, tax policy and practice, professional ethics, accounting education, and related topics. Without limiting the generality of the foregoing.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们