{"title":"不是你的普通公司:美国公司级投资的分位数回归方法","authors":"Doğuhan Sündal","doi":"10.1111/meca.12440","DOIUrl":null,"url":null,"abstract":"<p>A significant portion of the work published on firm investment adapts models that operate on an “average firm” assumption, which is different from the investment behavior of a modal firm. This study employs a Bayesian quantile regression model to explore the investment rates in the United States and finds, first, that the firms with higher investment rates have a higher responsiveness to the valuation ratio and lower responsiveness to the profit rate, and, second, that there is a decline in the responsiveness of firm investment to these factors in recent years. The paper also emphasizes the role of autonomous investments in determining firm-level investment rates, based on differing sectoral factors.</p>","PeriodicalId":46885,"journal":{"name":"Metroeconomica","volume":"74 4","pages":"858-886"},"PeriodicalIF":0.9000,"publicationDate":"2023-08-14","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/meca.12440","citationCount":"0","resultStr":"{\"title\":\"Not your average firm: A quantile regression approach to firm-level investment in the United States\",\"authors\":\"Doğuhan Sündal\",\"doi\":\"10.1111/meca.12440\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>A significant portion of the work published on firm investment adapts models that operate on an “average firm” assumption, which is different from the investment behavior of a modal firm. This study employs a Bayesian quantile regression model to explore the investment rates in the United States and finds, first, that the firms with higher investment rates have a higher responsiveness to the valuation ratio and lower responsiveness to the profit rate, and, second, that there is a decline in the responsiveness of firm investment to these factors in recent years. The paper also emphasizes the role of autonomous investments in determining firm-level investment rates, based on differing sectoral factors.</p>\",\"PeriodicalId\":46885,\"journal\":{\"name\":\"Metroeconomica\",\"volume\":\"74 4\",\"pages\":\"858-886\"},\"PeriodicalIF\":0.9000,\"publicationDate\":\"2023-08-14\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/meca.12440\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Metroeconomica\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/meca.12440\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Metroeconomica","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/meca.12440","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Not your average firm: A quantile regression approach to firm-level investment in the United States

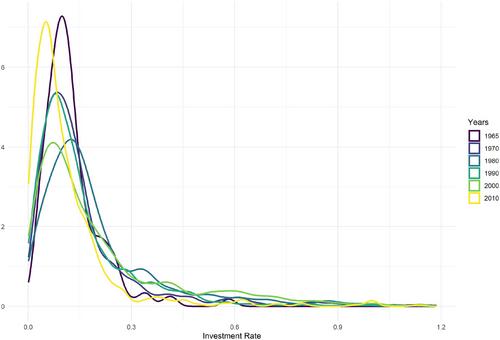

A significant portion of the work published on firm investment adapts models that operate on an “average firm” assumption, which is different from the investment behavior of a modal firm. This study employs a Bayesian quantile regression model to explore the investment rates in the United States and finds, first, that the firms with higher investment rates have a higher responsiveness to the valuation ratio and lower responsiveness to the profit rate, and, second, that there is a decline in the responsiveness of firm investment to these factors in recent years. The paper also emphasizes the role of autonomous investments in determining firm-level investment rates, based on differing sectoral factors.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们