{"title":"私募股权与地方公共财政","authors":"MARCEL OLBERT, PETER H. SEVERIN","doi":"10.1111/1475-679X.12487","DOIUrl":null,"url":null,"abstract":"<p>We study the economic impact of private equity (PE) investments on local governments, which are important corporate stakeholders. Examining over 11,000 deals and private firm data in Europe, we document that target firms' effective tax rates and total tax expenses decrease by 15% and 13% after PE deals. At the same time, target firms expand their capital expenditures and firm boundaries, but do not increase employment. Using administrative data on the public finances of German municipalities and exploiting the geographical and time-series variation in PE deals, we document that PE activity is negatively associated with local governments' tax revenues and spending. This result is likely driven by reduced tax payments of PE portfolio firms, accompanied by only modest positive spillovers of PE investments on regional economic growth. Collectively, our findings suggest that corporate tax efficiency serves as a cost-cutting channel in the PE sector and constrains the finances of local governments.</p>","PeriodicalId":48414,"journal":{"name":"Journal of Accounting Research","volume":"61 4","pages":"1313-1362"},"PeriodicalIF":6.3000,"publicationDate":"2023-05-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-679X.12487","citationCount":"0","resultStr":"{\"title\":\"Private Equity and Local Public Finances\",\"authors\":\"MARCEL OLBERT, PETER H. SEVERIN\",\"doi\":\"10.1111/1475-679X.12487\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We study the economic impact of private equity (PE) investments on local governments, which are important corporate stakeholders. Examining over 11,000 deals and private firm data in Europe, we document that target firms' effective tax rates and total tax expenses decrease by 15% and 13% after PE deals. At the same time, target firms expand their capital expenditures and firm boundaries, but do not increase employment. Using administrative data on the public finances of German municipalities and exploiting the geographical and time-series variation in PE deals, we document that PE activity is negatively associated with local governments' tax revenues and spending. This result is likely driven by reduced tax payments of PE portfolio firms, accompanied by only modest positive spillovers of PE investments on regional economic growth. Collectively, our findings suggest that corporate tax efficiency serves as a cost-cutting channel in the PE sector and constrains the finances of local governments.</p>\",\"PeriodicalId\":48414,\"journal\":{\"name\":\"Journal of Accounting Research\",\"volume\":\"61 4\",\"pages\":\"1313-1362\"},\"PeriodicalIF\":6.3000,\"publicationDate\":\"2023-05-11\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-679X.12487\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Accounting Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.12487\",\"RegionNum\":2,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.12487","RegionNum":2,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

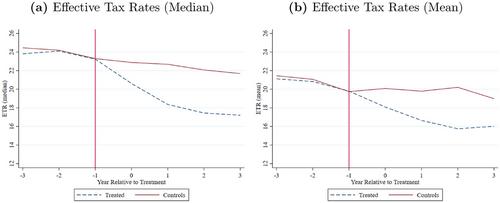

We study the economic impact of private equity (PE) investments on local governments, which are important corporate stakeholders. Examining over 11,000 deals and private firm data in Europe, we document that target firms' effective tax rates and total tax expenses decrease by 15% and 13% after PE deals. At the same time, target firms expand their capital expenditures and firm boundaries, but do not increase employment. Using administrative data on the public finances of German municipalities and exploiting the geographical and time-series variation in PE deals, we document that PE activity is negatively associated with local governments' tax revenues and spending. This result is likely driven by reduced tax payments of PE portfolio firms, accompanied by only modest positive spillovers of PE investments on regional economic growth. Collectively, our findings suggest that corporate tax efficiency serves as a cost-cutting channel in the PE sector and constrains the finances of local governments.

期刊介绍:

The Journal of Accounting Research is a general-interest accounting journal. It publishes original research in all areas of accounting and related fields that utilizes tools from basic disciplines such as economics, statistics, psychology, and sociology. This research typically uses analytical, empirical archival, experimental, and field study methods and addresses economic questions, external and internal, in accounting, auditing, disclosure, financial reporting, taxation, and information as well as related fields such as corporate finance, investments, capital markets, law, contracting, and information economics.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们