{"title":"调整后收益与未调整收益:德国大型上市公司形式调整的实证分析","authors":"Marcel Wiek, Korbinian Eichner","doi":"10.1002/jcaf.22611","DOIUrl":null,"url":null,"abstract":"<p>This article analyzes non-GAAP, pro forma earnings metrics of large German publicly traded companies to better understand their usage and relevance in practice. We base our analysis on a hand collected data set compiled from annual reports. Almost all companies in our data set use pro forma earnings. Typically, legal, restructuring, acquisition and accounting related costs get adjusted. EBIT, EBITDA, EPS and Net income are the most frequently adjusted earnings metrics. In almost all observed cases, pro forma earnings are higher than their underlying GAAP earnings. Our study addresses the challenge of investors to understand a company's “true” operating performance. Only when one understands the historically observable financial performance, one can make better predictions of its recurring, future financial performance. The article adds to the existing literature by analyzing in which part of the annual report pro forma earnings are typically disclosed, how transparent they are presented and reconciled, and what impact adjustments have compared to the unadjusted GAAP earnings.</p>","PeriodicalId":44561,"journal":{"name":"Journal of Corporate Accounting and Finance","volume":"34 3","pages":"47-63"},"PeriodicalIF":1.2000,"publicationDate":"2023-01-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jcaf.22611","citationCount":"1","resultStr":"{\"title\":\"Adjusted versus unadjusted earnings: An empirical analysis of pro forma adjustments in large German public companies\",\"authors\":\"Marcel Wiek, Korbinian Eichner\",\"doi\":\"10.1002/jcaf.22611\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This article analyzes non-GAAP, pro forma earnings metrics of large German publicly traded companies to better understand their usage and relevance in practice. We base our analysis on a hand collected data set compiled from annual reports. Almost all companies in our data set use pro forma earnings. Typically, legal, restructuring, acquisition and accounting related costs get adjusted. EBIT, EBITDA, EPS and Net income are the most frequently adjusted earnings metrics. In almost all observed cases, pro forma earnings are higher than their underlying GAAP earnings. Our study addresses the challenge of investors to understand a company's “true” operating performance. Only when one understands the historically observable financial performance, one can make better predictions of its recurring, future financial performance. The article adds to the existing literature by analyzing in which part of the annual report pro forma earnings are typically disclosed, how transparent they are presented and reconciled, and what impact adjustments have compared to the unadjusted GAAP earnings.</p>\",\"PeriodicalId\":44561,\"journal\":{\"name\":\"Journal of Corporate Accounting and Finance\",\"volume\":\"34 3\",\"pages\":\"47-63\"},\"PeriodicalIF\":1.2000,\"publicationDate\":\"2023-01-17\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jcaf.22611\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Corporate Accounting and Finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/jcaf.22611\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Corporate Accounting and Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/jcaf.22611","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Adjusted versus unadjusted earnings: An empirical analysis of pro forma adjustments in large German public companies

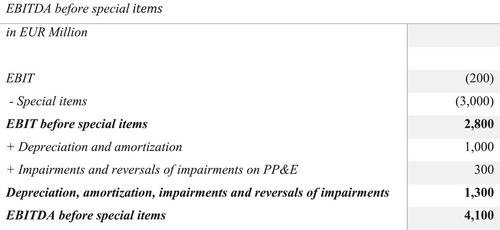

This article analyzes non-GAAP, pro forma earnings metrics of large German publicly traded companies to better understand their usage and relevance in practice. We base our analysis on a hand collected data set compiled from annual reports. Almost all companies in our data set use pro forma earnings. Typically, legal, restructuring, acquisition and accounting related costs get adjusted. EBIT, EBITDA, EPS and Net income are the most frequently adjusted earnings metrics. In almost all observed cases, pro forma earnings are higher than their underlying GAAP earnings. Our study addresses the challenge of investors to understand a company's “true” operating performance. Only when one understands the historically observable financial performance, one can make better predictions of its recurring, future financial performance. The article adds to the existing literature by analyzing in which part of the annual report pro forma earnings are typically disclosed, how transparent they are presented and reconciled, and what impact adjustments have compared to the unadjusted GAAP earnings.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们