Yong Tang, Jason Xiong, Zhitao Cheng, Yan Zhuang, Kunqi Li, Jingcong Xie, Yicheng Zhang

{"title":"从相关性和特征值视角看市场行为——基于RMT的中美市场调查。","authors":"Yong Tang, Jason Xiong, Zhitao Cheng, Yan Zhuang, Kunqi Li, Jingcong Xie, Yicheng Zhang","doi":"10.3390/e25101460","DOIUrl":null,"url":null,"abstract":"<p><p>This research systematically analyzes the behaviors of correlations among stock prices and the eigenvalues for correlation matrices by utilizing random matrix theory (RMT) for Chinese and US stock markets. Results suggest that most eigenvalues of both markets fall within the predicted distribution intervals by RMT, whereas some larger eigenvalues fall beyond the noises and carry market information. The largest eigenvalue represents the market and is a good indicator for averaged correlations. Further, the average largest eigenvalue shows similar movement with the index for both markets. The analysis demonstrates the fraction of eigenvalues falling beyond the predicted interval, pinpointing major market switching points. It has identified that the average of eigenvector components corresponds to the largest eigenvalue switch with the market itself. The investigation on the second largest eigenvalue and its eigenvector suggests that the Chinese market is dominated by four industries whereas the US market contains three leading industries. The study later investigates how it changes before and after a market crash, revealing that the two markets behave differently, and a major market structure change is observed in the Chinese market but not in the US market. The results shed new light on mining hidden information from stock market data.</p>","PeriodicalId":11694,"journal":{"name":"Entropy","volume":"25 10","pages":""},"PeriodicalIF":2.0000,"publicationDate":"2023-10-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10606484/pdf/","citationCount":"0","resultStr":"{\"title\":\"Looking into the Market Behaviors through the Lens of Correlations and Eigenvalues: An Investigation on the Chinese and US Markets Using RMT.\",\"authors\":\"Yong Tang, Jason Xiong, Zhitao Cheng, Yan Zhuang, Kunqi Li, Jingcong Xie, Yicheng Zhang\",\"doi\":\"10.3390/e25101460\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>This research systematically analyzes the behaviors of correlations among stock prices and the eigenvalues for correlation matrices by utilizing random matrix theory (RMT) for Chinese and US stock markets. Results suggest that most eigenvalues of both markets fall within the predicted distribution intervals by RMT, whereas some larger eigenvalues fall beyond the noises and carry market information. The largest eigenvalue represents the market and is a good indicator for averaged correlations. Further, the average largest eigenvalue shows similar movement with the index for both markets. The analysis demonstrates the fraction of eigenvalues falling beyond the predicted interval, pinpointing major market switching points. It has identified that the average of eigenvector components corresponds to the largest eigenvalue switch with the market itself. The investigation on the second largest eigenvalue and its eigenvector suggests that the Chinese market is dominated by four industries whereas the US market contains three leading industries. The study later investigates how it changes before and after a market crash, revealing that the two markets behave differently, and a major market structure change is observed in the Chinese market but not in the US market. The results shed new light on mining hidden information from stock market data.</p>\",\"PeriodicalId\":11694,\"journal\":{\"name\":\"Entropy\",\"volume\":\"25 10\",\"pages\":\"\"},\"PeriodicalIF\":2.0000,\"publicationDate\":\"2023-10-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10606484/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Entropy\",\"FirstCategoryId\":\"101\",\"ListUrlMain\":\"https://doi.org/10.3390/e25101460\",\"RegionNum\":3,\"RegionCategory\":\"物理与天体物理\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"PHYSICS, MULTIDISCIPLINARY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Entropy","FirstCategoryId":"101","ListUrlMain":"https://doi.org/10.3390/e25101460","RegionNum":3,"RegionCategory":"物理与天体物理","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"PHYSICS, MULTIDISCIPLINARY","Score":null,"Total":0}

Looking into the Market Behaviors through the Lens of Correlations and Eigenvalues: An Investigation on the Chinese and US Markets Using RMT.

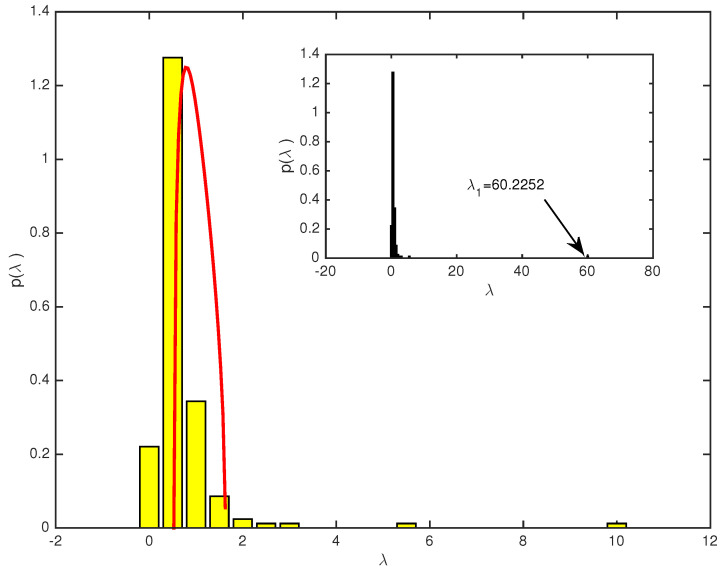

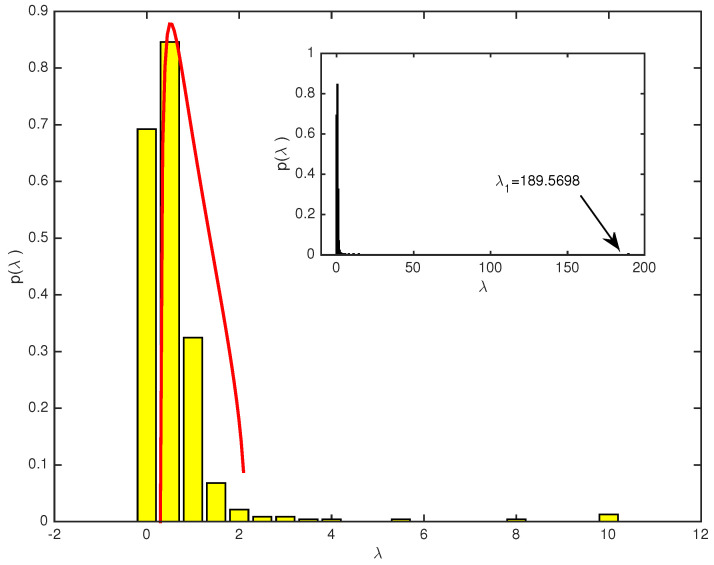

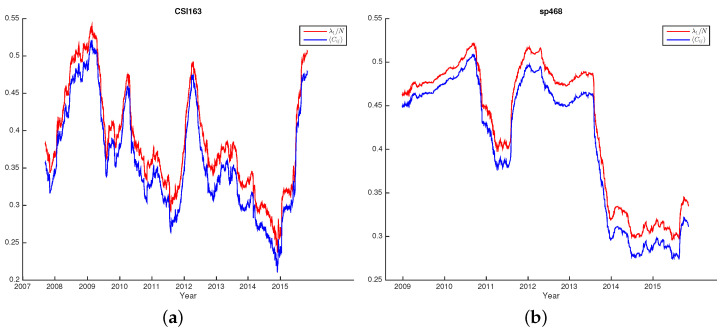

This research systematically analyzes the behaviors of correlations among stock prices and the eigenvalues for correlation matrices by utilizing random matrix theory (RMT) for Chinese and US stock markets. Results suggest that most eigenvalues of both markets fall within the predicted distribution intervals by RMT, whereas some larger eigenvalues fall beyond the noises and carry market information. The largest eigenvalue represents the market and is a good indicator for averaged correlations. Further, the average largest eigenvalue shows similar movement with the index for both markets. The analysis demonstrates the fraction of eigenvalues falling beyond the predicted interval, pinpointing major market switching points. It has identified that the average of eigenvector components corresponds to the largest eigenvalue switch with the market itself. The investigation on the second largest eigenvalue and its eigenvector suggests that the Chinese market is dominated by four industries whereas the US market contains three leading industries. The study later investigates how it changes before and after a market crash, revealing that the two markets behave differently, and a major market structure change is observed in the Chinese market but not in the US market. The results shed new light on mining hidden information from stock market data.

期刊介绍:

Entropy (ISSN 1099-4300), an international and interdisciplinary journal of entropy and information studies, publishes reviews, regular research papers and short notes. Our aim is to encourage scientists to publish as much as possible their theoretical and experimental details. There is no restriction on the length of the papers. If there are computation and the experiment, the details must be provided so that the results can be reproduced.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们