{"title":"以深化改革和全面开放推动稳定增长和高质量发展:展望、政策模拟与改革实施——上海财经大学宏观经济报告(2021-2022)总结","authors":"Kevin X. D. Huang, Guoqiang Tian, Lin Zhao","doi":"10.1002/ise3.2","DOIUrl":null,"url":null,"abstract":"<p>China's economy underwent a steady recovery in 2021. Investment grew steadily with structural improvement. Exports and imports surged while trade surplus expanded. On the other hand, although labor market conditions improved, income distribution worsened, contributing to sluggish growth in consumption, whereas the gap between consumer price index and producer price index widened, and the profits of enterprises of different sizes diverged, which may go beyond how they are correlated with the locations of the enterprises in the chain of production and trade. While proper liquidity was maintained with prudent monetary policy, risk spillover rose in the financial system, particularly for small and medium-sized banks. Household and local government debts remained at relatively high levels, further dragging down growth in consumption and infrastructure investment. The “dual carbon” goals exerted downward pressure on near-term growth in trading off their long-term benefits. The economy also faced challenges in its external environment in the midst of the prolonged COVID-19 pandemic aboard, trade protectionism, and the readjustment of the global value chain. Moreover, excessive supervision and inadequate implementation disturbed China's economy, resulting in declined market vitality and confidence of market participants. Based on the Institute for Advanced Research-China Macroeconomic Model, the baseline real gross domestic product growth rate is projected to be 5.5% in 2022. Alternative scenario analyses and policy simulations are conducted, in addition to the benchmark forecast, to reflect the influences of various risks and possible favorable situations. The findings suggest that China should deepen reform and open up more comprehensively and initiatively, while special effort should be placed on providing accommodative policy and friendly public opinion environment, to facilitate steady growth and propel high-quality development. A comprehensive macroeconomic governance framework with Chinese characteristics must be developed from systems thinking, to resolve the various issues, internal and external, cyclical and secular, structural and institutional, in an all-inclusive and coherent manner.</p>","PeriodicalId":29662,"journal":{"name":"International Studies of Economics","volume":"17 1","pages":"2-20"},"PeriodicalIF":0.5000,"publicationDate":"2022-07-03","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ise3.2","citationCount":"1","resultStr":"{\"title\":\"Propelling steady growth and high-quality development through deeper reform and more comprehensive opening up: Outlook, policy simulations, and reform implementation—A summary of the Annual SUFE Macroeconomic Report (2021–2022)\",\"authors\":\"Kevin X. D. Huang, Guoqiang Tian, Lin Zhao\",\"doi\":\"10.1002/ise3.2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>China's economy underwent a steady recovery in 2021. Investment grew steadily with structural improvement. Exports and imports surged while trade surplus expanded. On the other hand, although labor market conditions improved, income distribution worsened, contributing to sluggish growth in consumption, whereas the gap between consumer price index and producer price index widened, and the profits of enterprises of different sizes diverged, which may go beyond how they are correlated with the locations of the enterprises in the chain of production and trade. While proper liquidity was maintained with prudent monetary policy, risk spillover rose in the financial system, particularly for small and medium-sized banks. Household and local government debts remained at relatively high levels, further dragging down growth in consumption and infrastructure investment. The “dual carbon” goals exerted downward pressure on near-term growth in trading off their long-term benefits. The economy also faced challenges in its external environment in the midst of the prolonged COVID-19 pandemic aboard, trade protectionism, and the readjustment of the global value chain. Moreover, excessive supervision and inadequate implementation disturbed China's economy, resulting in declined market vitality and confidence of market participants. Based on the Institute for Advanced Research-China Macroeconomic Model, the baseline real gross domestic product growth rate is projected to be 5.5% in 2022. Alternative scenario analyses and policy simulations are conducted, in addition to the benchmark forecast, to reflect the influences of various risks and possible favorable situations. The findings suggest that China should deepen reform and open up more comprehensively and initiatively, while special effort should be placed on providing accommodative policy and friendly public opinion environment, to facilitate steady growth and propel high-quality development. A comprehensive macroeconomic governance framework with Chinese characteristics must be developed from systems thinking, to resolve the various issues, internal and external, cyclical and secular, structural and institutional, in an all-inclusive and coherent manner.</p>\",\"PeriodicalId\":29662,\"journal\":{\"name\":\"International Studies of Economics\",\"volume\":\"17 1\",\"pages\":\"2-20\"},\"PeriodicalIF\":0.5000,\"publicationDate\":\"2022-07-03\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/ise3.2\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"International Studies of Economics\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/ise3.2\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q4\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Studies of Economics","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/ise3.2","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"ECONOMICS","Score":null,"Total":0}

Propelling steady growth and high-quality development through deeper reform and more comprehensive opening up: Outlook, policy simulations, and reform implementation—A summary of the Annual SUFE Macroeconomic Report (2021–2022)

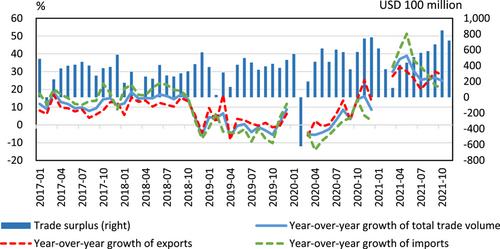

China's economy underwent a steady recovery in 2021. Investment grew steadily with structural improvement. Exports and imports surged while trade surplus expanded. On the other hand, although labor market conditions improved, income distribution worsened, contributing to sluggish growth in consumption, whereas the gap between consumer price index and producer price index widened, and the profits of enterprises of different sizes diverged, which may go beyond how they are correlated with the locations of the enterprises in the chain of production and trade. While proper liquidity was maintained with prudent monetary policy, risk spillover rose in the financial system, particularly for small and medium-sized banks. Household and local government debts remained at relatively high levels, further dragging down growth in consumption and infrastructure investment. The “dual carbon” goals exerted downward pressure on near-term growth in trading off their long-term benefits. The economy also faced challenges in its external environment in the midst of the prolonged COVID-19 pandemic aboard, trade protectionism, and the readjustment of the global value chain. Moreover, excessive supervision and inadequate implementation disturbed China's economy, resulting in declined market vitality and confidence of market participants. Based on the Institute for Advanced Research-China Macroeconomic Model, the baseline real gross domestic product growth rate is projected to be 5.5% in 2022. Alternative scenario analyses and policy simulations are conducted, in addition to the benchmark forecast, to reflect the influences of various risks and possible favorable situations. The findings suggest that China should deepen reform and open up more comprehensively and initiatively, while special effort should be placed on providing accommodative policy and friendly public opinion environment, to facilitate steady growth and propel high-quality development. A comprehensive macroeconomic governance framework with Chinese characteristics must be developed from systems thinking, to resolve the various issues, internal and external, cyclical and secular, structural and institutional, in an all-inclusive and coherent manner.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们