Casey Michelle Haining, Jane Tiller, Margaret Otlowski, Penny Gleeson, Carsten Murawski, Kristine Barlow-Stewart, Paul Lacaze, Aideen McInerney-Leo, Louise Anne Keogh

{"title":"财务顾问和主要线人对澳大利亚行业主导的暂停人寿保险基因测试的看法。","authors":"Casey Michelle Haining, Jane Tiller, Margaret Otlowski, Penny Gleeson, Carsten Murawski, Kristine Barlow-Stewart, Paul Lacaze, Aideen McInerney-Leo, Louise Anne Keogh","doi":"10.1159/000533532","DOIUrl":null,"url":null,"abstract":"<p><strong>Introduction: </strong>Genetic discrimination (GD) in the context of life insurance is a perennial concern in Australia and internationally. To address such concerns in Australia, an industry self-regulated Moratorium on Genetic Tests in Life Insurance was introduced in 2019 to restrict life insurers from using genetic test results in underwriting for policies under certain limits. Financial advisers (FAs) are sometimes engaged by clients to provide financial advice and assist them to apply for life insurance. They are therefore well-placed to comment on GD and the operation of the Moratorium. Despite this, the financial advising sector in Australia has yet to be studied empirically with regards to GD and the Moratorium. This study aims to capture this perspective by reporting on interviews with the financial advising sector.</p><p><strong>Methods: </strong>Ten semi-structured qualitative interviews were conducted with FAs and key informants and were analysed using thematic analysis.</p><p><strong>Conclusion(s): </strong>Participants' level of awareness and understanding of the Moratorium varied. Participants reported mixed views on the Moratorium's effectiveness, how it operates in practice, and perceived industry compliance. Participants also provided reflections on Australia's current approach to regulating GD, with most participants supporting the concept of industry self-regulation but identifying a need for this to be supplemented with external oversight and meaningful recourse mechanisms for consumers. Our results suggest that there is scope to increase FAs' awareness of GD, and that further research, consultation, and policy consideration are required to identify an optimal regulatory response to GD in Australia.</p>","PeriodicalId":49650,"journal":{"name":"Public Health Genomics","volume":" ","pages":"123-134"},"PeriodicalIF":1.5000,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10614474/pdf/","citationCount":"0","resultStr":"{\"title\":\"Financial Advisers' and Key Informants' Perspectives on the Australian Industry-Led Moratorium on Genetic Tests in Life Insurance.\",\"authors\":\"Casey Michelle Haining, Jane Tiller, Margaret Otlowski, Penny Gleeson, Carsten Murawski, Kristine Barlow-Stewart, Paul Lacaze, Aideen McInerney-Leo, Louise Anne Keogh\",\"doi\":\"10.1159/000533532\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><strong>Introduction: </strong>Genetic discrimination (GD) in the context of life insurance is a perennial concern in Australia and internationally. To address such concerns in Australia, an industry self-regulated Moratorium on Genetic Tests in Life Insurance was introduced in 2019 to restrict life insurers from using genetic test results in underwriting for policies under certain limits. Financial advisers (FAs) are sometimes engaged by clients to provide financial advice and assist them to apply for life insurance. They are therefore well-placed to comment on GD and the operation of the Moratorium. Despite this, the financial advising sector in Australia has yet to be studied empirically with regards to GD and the Moratorium. This study aims to capture this perspective by reporting on interviews with the financial advising sector.</p><p><strong>Methods: </strong>Ten semi-structured qualitative interviews were conducted with FAs and key informants and were analysed using thematic analysis.</p><p><strong>Conclusion(s): </strong>Participants' level of awareness and understanding of the Moratorium varied. Participants reported mixed views on the Moratorium's effectiveness, how it operates in practice, and perceived industry compliance. Participants also provided reflections on Australia's current approach to regulating GD, with most participants supporting the concept of industry self-regulation but identifying a need for this to be supplemented with external oversight and meaningful recourse mechanisms for consumers. Our results suggest that there is scope to increase FAs' awareness of GD, and that further research, consultation, and policy consideration are required to identify an optimal regulatory response to GD in Australia.</p>\",\"PeriodicalId\":49650,\"journal\":{\"name\":\"Public Health Genomics\",\"volume\":\" \",\"pages\":\"123-134\"},\"PeriodicalIF\":1.5000,\"publicationDate\":\"2023-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10614474/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Public Health Genomics\",\"FirstCategoryId\":\"3\",\"ListUrlMain\":\"https://doi.org/10.1159/000533532\",\"RegionNum\":4,\"RegionCategory\":\"医学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2023/8/14 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"Q4\",\"JCRName\":\"GENETICS & HEREDITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Public Health Genomics","FirstCategoryId":"3","ListUrlMain":"https://doi.org/10.1159/000533532","RegionNum":4,"RegionCategory":"医学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2023/8/14 0:00:00","PubModel":"Epub","JCR":"Q4","JCRName":"GENETICS & HEREDITY","Score":null,"Total":0}

Financial Advisers' and Key Informants' Perspectives on the Australian Industry-Led Moratorium on Genetic Tests in Life Insurance.

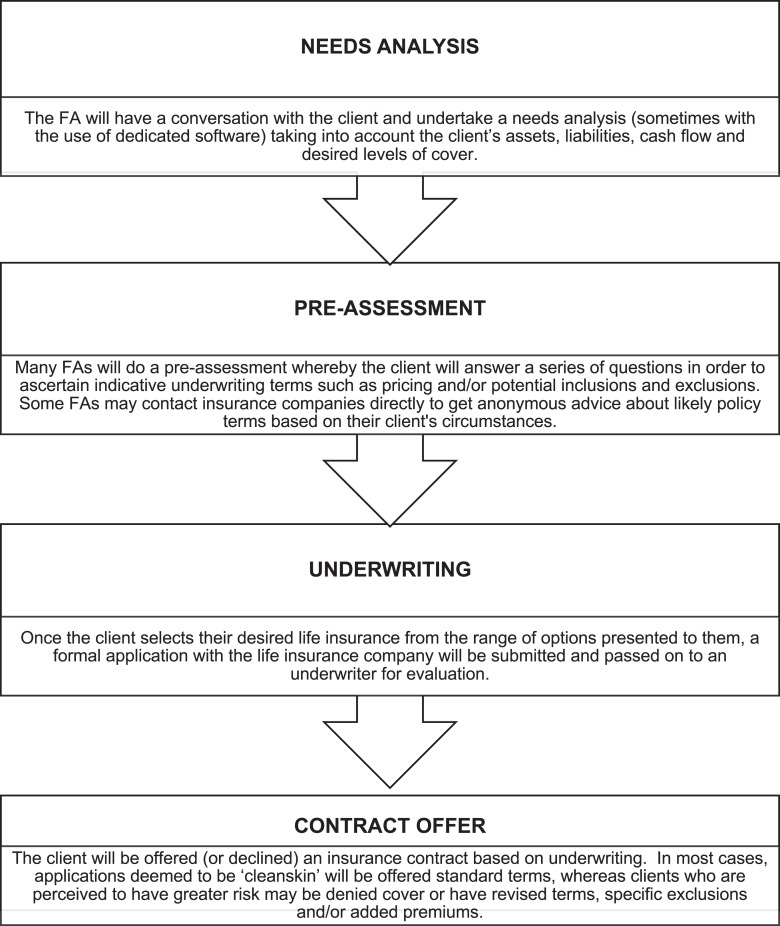

Introduction: Genetic discrimination (GD) in the context of life insurance is a perennial concern in Australia and internationally. To address such concerns in Australia, an industry self-regulated Moratorium on Genetic Tests in Life Insurance was introduced in 2019 to restrict life insurers from using genetic test results in underwriting for policies under certain limits. Financial advisers (FAs) are sometimes engaged by clients to provide financial advice and assist them to apply for life insurance. They are therefore well-placed to comment on GD and the operation of the Moratorium. Despite this, the financial advising sector in Australia has yet to be studied empirically with regards to GD and the Moratorium. This study aims to capture this perspective by reporting on interviews with the financial advising sector.

Methods: Ten semi-structured qualitative interviews were conducted with FAs and key informants and were analysed using thematic analysis.

Conclusion(s): Participants' level of awareness and understanding of the Moratorium varied. Participants reported mixed views on the Moratorium's effectiveness, how it operates in practice, and perceived industry compliance. Participants also provided reflections on Australia's current approach to regulating GD, with most participants supporting the concept of industry self-regulation but identifying a need for this to be supplemented with external oversight and meaningful recourse mechanisms for consumers. Our results suggest that there is scope to increase FAs' awareness of GD, and that further research, consultation, and policy consideration are required to identify an optimal regulatory response to GD in Australia.

期刊介绍:

''Public Health Genomics'' is the leading international journal focusing on the timely translation of genome-based knowledge and technologies into public health, health policies, and healthcare as a whole. This peer-reviewed journal is a bimonthly forum featuring original papers, reviews, short communications, and policy statements. It is supplemented by topic-specific issues providing a comprehensive, holistic and ''all-inclusive'' picture of the chosen subject. Multidisciplinary in scope, it combines theoretical and empirical work from a range of disciplines, notably public health, molecular and medical sciences, the humanities and social sciences. In so doing, it also takes into account rapid scientific advances from fields such as systems biology, microbiomics, epigenomics or information and communication technologies as well as the hight potential of ''big data'' for public health.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们