{"title":"Nowcasting India's Quarterly GDP Growth: A Factor-Augmented Time-Varying Coefficient Regression Model (FA-TVCRM).","authors":"Rudrani Bhattacharya, Bornali Bhandari, Sudipto Mundle","doi":"10.1007/s40953-022-00335-6","DOIUrl":null,"url":null,"abstract":"<p><p>Governments, central banks, private firms and others need high frequency information on the state of the economy for their decision making. However, a key indicator like GDP is only available quarterly and that too with a lag. Hence decision makers use high frequency daily, weekly or monthly information to project GDP growth in a given quarter. This method, known as nowcasting, started out in advanced country central banks using bridge models. Nowcasting is now based on more advanced techniques, mostly dynamic factor models. In this paper we use a novel approach, a Factor Augmented Time Varying Coefficient Regression (FA-TVCR) model, which allows us to extract information from a large number of high frequency indicators and at the same time inherently addresses the issue of frequent structural breaks encountered in Indian GDP growth. One specification of the FA-TVCR model is estimated using 19 variables available for a long period starting in 2007-08:Q1. Another specification estimates the model using a larger set of 28 indicators available for a shorter period starting in 2015-16:Q1. Comparing our model with two alternative models, we find that the FA-TVCR model outperforms a Dynamic Factor Model (DFM) model and a univariate Autoregressive Integrated Moving Average (ARIMA) model in terms of both in-sample and out-of-sample Root Mean Square Error (RMSE). Further, comparing the predictive power of the three models using the Diebold-Mariano test, we find that FA-TVCR model outperforms DFM consistently. In terms of out-of-sample forecast accuracy both the FA-TVCR model and the ARIMA model have the same predictive accuracy under normal conditions. However, the FA-TVCR model outperforms the ARIMA model when applied for nowcasting in periods of major shocks like the Covid-19 shock of 2020-21.</p>","PeriodicalId":73920,"journal":{"name":"","volume":"21 1","pages":"213-234"},"PeriodicalIF":0.0,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9838450/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s40953-022-00335-6","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 0

Abstract

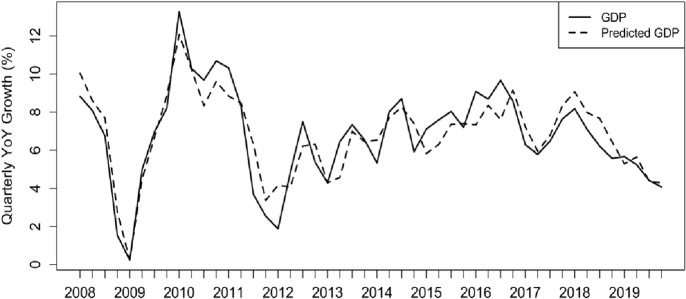

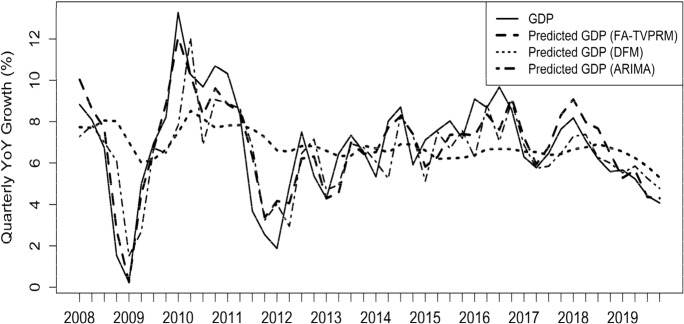

Governments, central banks, private firms and others need high frequency information on the state of the economy for their decision making. However, a key indicator like GDP is only available quarterly and that too with a lag. Hence decision makers use high frequency daily, weekly or monthly information to project GDP growth in a given quarter. This method, known as nowcasting, started out in advanced country central banks using bridge models. Nowcasting is now based on more advanced techniques, mostly dynamic factor models. In this paper we use a novel approach, a Factor Augmented Time Varying Coefficient Regression (FA-TVCR) model, which allows us to extract information from a large number of high frequency indicators and at the same time inherently addresses the issue of frequent structural breaks encountered in Indian GDP growth. One specification of the FA-TVCR model is estimated using 19 variables available for a long period starting in 2007-08:Q1. Another specification estimates the model using a larger set of 28 indicators available for a shorter period starting in 2015-16:Q1. Comparing our model with two alternative models, we find that the FA-TVCR model outperforms a Dynamic Factor Model (DFM) model and a univariate Autoregressive Integrated Moving Average (ARIMA) model in terms of both in-sample and out-of-sample Root Mean Square Error (RMSE). Further, comparing the predictive power of the three models using the Diebold-Mariano test, we find that FA-TVCR model outperforms DFM consistently. In terms of out-of-sample forecast accuracy both the FA-TVCR model and the ARIMA model have the same predictive accuracy under normal conditions. However, the FA-TVCR model outperforms the ARIMA model when applied for nowcasting in periods of major shocks like the Covid-19 shock of 2020-21.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们