{"title":"Examining the Time Varying Spillover Dynamics of Indian Financial Indictors from Global and Local Economic Uncertainty.","authors":"Pawan Kumar, Vipul Kumar Singh","doi":"10.1007/s40953-022-00333-8","DOIUrl":null,"url":null,"abstract":"<p><p>The research aims to excavate the role of global (Fed Rate, Crude, Real Dollar Index) and endogenous economic variables (GDP and Consumer Price Index) in shaping the spillover amongst the major Indian Financial indicators, viz. Nifty Index, MCX Gold, USDINR, Govt. Bond 10Y maturity and agricultural index N-Krishi. To facilitate cross-comparison decomposition of time-varying spillover output generated from Time-Varying Vector Autoregression (TVP-VAR) with aggregation at three layers is performed. The research finds that Indian Financial Indicators are vulnerable to spillover shocks from global variables predominantly driven by Fed Rate and Real Dollar Index. USDINR turns out to be most sensitive to global shocks and transgresses the shock to other financial indicators. Importantly, persistently high inflation has brought volatility spikes in the directional spillover to financial indicators. Though spillover subsidence is observed post-2014, with an all-time high during GFC, a sudden spurt in all financial indicators has been observed post-Covid-19, with Govt. bonds showing a sporadic rise. An important observation relates to staunch spillover from GDP during GFC with reoccurrence post-Covid. Additionally, a closely knit spillover tie is observed among USDINR, N-Krishi, and Crude. The study is beneficial to RBI to proactively monitor the weakening rupee along with Fed tapering to manage the rising spillover post-Covid-19. The effort of RBI has to be reciprocated by the government in inflation targeting to reinforce the curbing efforts of rising shock spillover.</p>","PeriodicalId":73920,"journal":{"name":"","volume":"21 1","pages":"99-121"},"PeriodicalIF":0.0,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9758468/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s40953-022-00333-8","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 0

Abstract

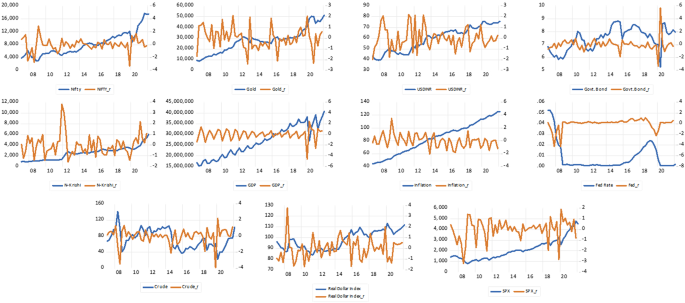

The research aims to excavate the role of global (Fed Rate, Crude, Real Dollar Index) and endogenous economic variables (GDP and Consumer Price Index) in shaping the spillover amongst the major Indian Financial indicators, viz. Nifty Index, MCX Gold, USDINR, Govt. Bond 10Y maturity and agricultural index N-Krishi. To facilitate cross-comparison decomposition of time-varying spillover output generated from Time-Varying Vector Autoregression (TVP-VAR) with aggregation at three layers is performed. The research finds that Indian Financial Indicators are vulnerable to spillover shocks from global variables predominantly driven by Fed Rate and Real Dollar Index. USDINR turns out to be most sensitive to global shocks and transgresses the shock to other financial indicators. Importantly, persistently high inflation has brought volatility spikes in the directional spillover to financial indicators. Though spillover subsidence is observed post-2014, with an all-time high during GFC, a sudden spurt in all financial indicators has been observed post-Covid-19, with Govt. bonds showing a sporadic rise. An important observation relates to staunch spillover from GDP during GFC with reoccurrence post-Covid. Additionally, a closely knit spillover tie is observed among USDINR, N-Krishi, and Crude. The study is beneficial to RBI to proactively monitor the weakening rupee along with Fed tapering to manage the rising spillover post-Covid-19. The effort of RBI has to be reciprocated by the government in inflation targeting to reinforce the curbing efforts of rising shock spillover.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们