{"title":"Treatment of Accounting Changes and Covenant Violation Errors","authors":"CHUNMEI ZHU","doi":"10.1111/1475-679X.12515","DOIUrl":null,"url":null,"abstract":"<p>GAAP provisions in loan contracts specify how to address the effect of accounting changes on financial covenants. I document a pronounced upward trend in and the dominance of frozen-on-request (FOR) GAAP provisions, which incorporate accounting changes unless either the borrower or the lender requests a freeze. FOR GAAP streamlines the process of incorporating accounting changes into covenant calculations by obviating the need for renegotiations and prevents opportunistic GAAP freezes by requiring good faith renegotiations. Therefore, FOR GAAP is more likely to incorporate accounting changes beneficial to covenant informativeness, leading to lower false positives (i.e., Type I errors of financial covenant violations) and false negatives (i.e., Type II errors of financial covenant violations). Based on a large sample of loan contracts, I find that FOR GAAP decreases false positives and false negatives after controlling for self-selection bias and that the decrease is more pronounced when accounting changes relevant to financial covenants are more significant. My study provides new evidence of the role accounting standards and GAAP provisions play in debt contracting efficiency.</p>","PeriodicalId":48414,"journal":{"name":"Journal of Accounting Research","volume":"62 2","pages":"783-824"},"PeriodicalIF":6.3000,"publicationDate":"2023-10-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-679X.12515","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.12515","RegionNum":2,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

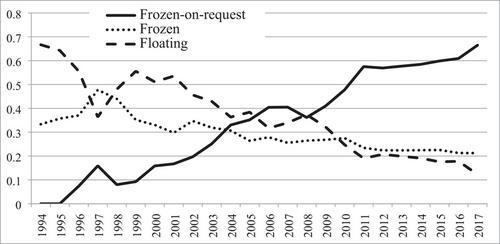

Abstract

GAAP provisions in loan contracts specify how to address the effect of accounting changes on financial covenants. I document a pronounced upward trend in and the dominance of frozen-on-request (FOR) GAAP provisions, which incorporate accounting changes unless either the borrower or the lender requests a freeze. FOR GAAP streamlines the process of incorporating accounting changes into covenant calculations by obviating the need for renegotiations and prevents opportunistic GAAP freezes by requiring good faith renegotiations. Therefore, FOR GAAP is more likely to incorporate accounting changes beneficial to covenant informativeness, leading to lower false positives (i.e., Type I errors of financial covenant violations) and false negatives (i.e., Type II errors of financial covenant violations). Based on a large sample of loan contracts, I find that FOR GAAP decreases false positives and false negatives after controlling for self-selection bias and that the decrease is more pronounced when accounting changes relevant to financial covenants are more significant. My study provides new evidence of the role accounting standards and GAAP provisions play in debt contracting efficiency.

期刊介绍:

The Journal of Accounting Research is a general-interest accounting journal. It publishes original research in all areas of accounting and related fields that utilizes tools from basic disciplines such as economics, statistics, psychology, and sociology. This research typically uses analytical, empirical archival, experimental, and field study methods and addresses economic questions, external and internal, in accounting, auditing, disclosure, financial reporting, taxation, and information as well as related fields such as corporate finance, investments, capital markets, law, contracting, and information economics.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们