{"title":"The Fragile Link: Supply Chain Disruptions and Global Food Security","authors":"","doi":"10.1002/fsat.3803_9.x","DOIUrl":null,"url":null,"abstract":"<p><b><i>Maria Masoura outlines the drivers of supply chain disruption and their ripple effects on global food security</i>.</b></p><p>The Food and Agriculture Organization (FAO) defines food security as when all people, at all times, have physical and economic access to sufficient safe and nutritious food that meets their dietary needs and food preferences for an active and healthy life. Currently, global food security is under pressure due to a combination of unprecedented pandemic threats and their consequences, climate change, economic disparities, and ongoing conflicts that strain supply chains and threaten the global integral right to food. The FAO, in conjunction with the World Food Programme (WFP), highlighted an intensifying crisis of food insecurity in their most recent Hunger Hotspots report, pinpointing eighteen areas of critical concern, with Mali, the Palestinian Territories, and (South) Sudan drawing particular attention. Haiti has been identified as a new area of concern due to escalating violence by non-state armed groups<sup>(</sup><span><sup>1</sup></span><sup>)</sup>. The Integrated Food Security Phase Classification (IPC) has verified that in Gaza, 96% of the population, or approximately 2.15 million individuals, are grappling with severe food insecurity (at or above IPC Phase 3), and of these, 495,000 are enduring extreme food scarcity (IPC Phase 5) as projected through September 2024<sup>(</sup><span><sup>2</sup></span><sup>)</sup>. The Agricultural Market Information System (AMIS) Market Monitor report from June 2024 has indicated that wheat yields are likely to be adversely affected by unfavourable climatic conditions, such as drought and extended periods of frost, particularly in pivotal agricultural regions of Russia. This situation is expected to lead to further escalations in prices, exacerbated by limitations in production and delays in transportation, especially within the Black Sea vicinity<sup>(</sup><span><sup>3</sup></span><sup>)</sup>. In the wake of the ongoing Ukraine-Russia conflict, the global food crisis is worsened due to the growing number of food and fertilizer trade restrictions being put in place by countries to increase domestic supply and reduce prices. All these coupled with weather extremes, shipping delays, and relapsing pandemic waves further affect the already fragile food systems especially when limited substitutes exist for staple foods. This article provides an overview of the drivers of food insecurity and their direct consequences.</p><p>Rice, wheat, maize, and soybeans are the cornerstone crops of the global diet, accounting for nearly half of caloric intake, with rice and wheat alone making up 19% and 18%, respectively. A significant 60% of the world's food production occurs in just five countries: China, the United States, India, Brazil, and Argentina. Within these countries, certain areas are pivotal for production; for instance, five states in India are responsible for 88% of its wheat output, while 61% of the United States’ maize is produced by five states in the Midwest. This geographic concentration makes a substantial segment of the world's food supply susceptible to a range of factors that can disrupt the continuity of food production and distribution<sup>(</sup><span><sup>4</sup></span><sup>)</sup>. Ukraine <i>was</i> known as the ‘breadbasket of Europe’ ranking among the top three global exporters of corn, wheat, barley, sunflower oil, and mineral fertilizers, while the developed agriculture <i>made</i> that country one of the top consumers of pesticides (around 125,000 tons a year). Geopolitical events (e.g. conflicts), climate extremes, pandemics, regulatory changes, sociological and technological pressures, economic factors (unemployment, rising food prices) growing inequality are among the most common drivers that put pressure on the supply chain and threaten global food security (Figure 1).</p><p>Worldwide, peace-making is in crisis and 2024 began with the ten active battlefields, among them: Gaza, Sudan, and Ukraine. The ‘paradigm’ of Russia's invasion of Ukraine is an unfortunate, still real scenario of how armed conflicts, including population displacement, destruction of food systems (e.g. land, infrastructure, etc.), and restricted humanitarian aid drive acute food insecurity in many geographical hotspots. As for today, the war in Ukraine, along with the ongoing issues in the Black Sea - a critical supply and transit hub for commodities and agricultural inputs – is having a significant economic and humanitarian impact. This situation is continuously getting worse due to the combined effects of weather extremes.</p><p>Since the onset of the war, Ukrainian farmers could not use their lands in occupied regions like Donetsk, Luhansk, Kherson, and Zaporizhzhia. Hence, production, trading, and supply of critical commodities (e.g. wheat, barley, sunflower oil) have been hampered. Ukraine, once a major supplier to the World Food Programme (WFP), now finds itself in need of assistance to meet its own food requirements. While several countries (e.g. US, UK, EU, Australia, Canada, and Japan) imposed sanctions on Russia, the latter found ways around such regimes and ’replied’ by embargoing exports of over 200 products (e.g. electronics, medical, agricultural, etc.) to nations it considers hostile, by shifting exports to China and India, redirecting its trade towards China and India, and closing the Nord Stream 1 pipeline, which was a primary source of Germany's natural gas. All that has made the import of crucial commodities (including oil, gas, fertilizers, and wheat) to the EU scarce and inflated prices while domestic food production slowed down in both the EU and China due to the record-high price of natural gas used to make fertilizers. Of note, fertilizer prices increased globally by 30% by early 2022 after experiencing an 80% hike in 2021 and the surging gas prices increased freight costs for all modes of transportation<sup>(</sup><span><sup>5</sup></span><sup>)</sup>. This, in turn, caused delays and backlogs for industries, creating long and short-term ripples across supply chains, and affecting product quality.</p><p>Since the onset of the war, multiple attacks on the port of Odessa and sanctions on Russian vessels entering the UK, USA, and EU ports disrupted shipping, spiked freight rates, and suspended services to other longer sea routes. Upon the Middle East conflict, more attacks, on commercial vessels in the Red Sea region which extended to the Arabian Gulf, threatened oil shipments. Trading in the region of Israeli southern ports, especially Ashkelon and Ashdod faced heightened risk due to a missile attack and the closure of Ashkelon. Since November 2023, intensified assaults by Houthi forces on vessels destined for the Suez Canal have caused them to divert to a longer passage around the southern tip of Africa with multiple impacts such as rising costs, global delays and disruptions, and the increase of greenhouse gas (GHG) emissions. Russia also closed its airspace to European and U.S. airlines, forcing some long-haul flights to Asia to take longer routes (therefore increasing GHG emissions).</p><p>The contamination of air, water, livestock, and soil with munition debris, explosive remnants of war (ERW), and hazardous substances directly affects food safety and human health. Missile and air strikes in many parts of the country (Donetsk, Kharkiv, Chernihiv, Kyiv, Makariv, and Mariupol among them) resulted in massive widespread debris (e.g. asbestos used in more than 50% of infrastructure) while the supply of drinking water has been affected by hostilities in water pipelines and wastewater treatment stations. Potentially the most significant risk to humans is the exposure to chemical vapours (e.g. benzene, toluene, naphthalene, hydrogen sulphide, mercaptan, hydrocyanic acid, ammonia, PAHs, particulate matter, black carbon, aerosols, and a variety of gases, oils and fuel spills) resulted from fires/explosions to chemical industries and fuel infrastructure. Equally, munition debris (e.g. depleted uranium, explosives, heavy metals, unexploded ordnance, and landmines) contaminate agricultural land, drinking water, ecological habitats, flora, and fauna. Considering the fate of these harmful chemical deposits, ‘after-war’ agriculture in these fields is thought to be impossible to resume.</p><p>The ten warmest years in the 174-year record have all occurred during the last decade (2014–2023)<sup>(</sup><span><sup>6</sup></span><sup>)</sup>. Crop production is highly sensitive to climate variability and is affected by weather extremes (e.g. temperature, heavy precipitation (including river floods), droughts, and storms (including tropical cyclones). Anthropogenic activity, particularly the expansion of crop and irrigation, industrialization, and transport (e.g. air/sea/land shipping), that increases GHG, and high aerosol concentrations, is the main driver of such phenomena. Although not all crops are equally vulnerable to climate change, increased atmospheric carbon dioxide (CO<sub>2</sub>), rising temperature, and changes in precipitation regimes, affect their yield, nutritional content, physical strength, and marketability. For instance, extended periods of drought can lead to crop failures. It is anticipated that C<sub>3</sub> plants, when grown in environments with high CO<sub>2</sub> concentrations, will exhibit reduced levels of proteins, minerals, and essential micronutrients like zinc and iron. Elevated temperatures can cause an uptick in respiration rates, which in turn diminishes the sugar content of the crops when harvested. Moreover, such climatic alterations make the crops more susceptible to pests and diseases, affecting them both in the fields and during storage. For example, plants that endure water saturation are more susceptible to viral infections, whereas those experiencing drought conditions struggle more to compete with weeds for soil moisture and nutrients<sup>(</sup><span><sup>7</sup></span><sup>)</sup>.</p><p>High temperatures (average increase of 1.5°C) and low/unreliable rainfall will impact the global production of maize, rice, and potato which is expected to decrease in all breadbasket countries while utilization shows the opposite trend. For maize, the common responses to drought are a decrease in leaf number, abnormal root formation, slow growth rate, and lower chlorophyll content. In China, severe drought reduced maize yield by up to 14%<sup>(</sup><span><sup>2</sup></span><sup>)</sup>.</p><p>The COVID-19 pandemic has doubled the severity of food insecurity, now affecting 811 million people worldwide. The crisis occurred initially due to the decline in food production and processing, limited access to critical inputs, and trade restrictions (e.g., transport delay of seeds and fertilizers slowed down the global agricultural process). Additionally, reduced labour (e.g., unemployment, social distancing measures, infections, and more limited transport systems) contributed to the instability, culminating in price surges even for staple foods.</p><p>This was compounded by the war in Ukraine that disrupted almost a third of the world's wheat market.</p><p>Geopolitical tensions, climate change, and extreme weather, all culminating in the wake of the pandemic, are tilting global food security into a high-risk state due to the vulnerability of staple food production, supply, and lack/limited substitutes. The ongoing conflicts in Ukraine and the Middle East battlefields have profound impacts on global food production and supplies, with far-reaching consequences for hunger and food security across the world. As of June 2024, 16 countries had implemented 22 food export bans, and 8 had implemented 15 export-limiting measures in major food commodities (e.g., wheat, soybean, rice, sugar, vegetable oils, etc.) while food inflation has increased between 5 and 30 per cent (or more) in most of the low- and middle-income countries<sup>(</sup><span><sup>8</sup></span><sup>)</sup>. In particular, production and trade of wheat, maize, and rice in 2024 decreased and are forecast to decline below the 2023 level by 1.1 per cent. Further reductions in the crop yield are expected in light of La Niña (La Niña is also sometimes called El Viejo, or simply ‘a cold event’), predicted to dominate from August to October 2024 and persist through December 2024 to February 2025, which is thought to significantly change global weather patterns by influencing rainfall distribution and temperatures. Although it elevates the risk of flooding in vulnerable areas globally, it might also offer beneficial relief to certain regions, improving agricultural prospects<sup>(</sup><span><sup>9</sup></span><sup>)</sup>.</p><p>FAO's 2024/2025 recent projections indicate a rise in production and an uptick in the final inventories of various staple commodities (Figure 2). Yet, the resilience of the global food production and distribution systems continues to be threatened by the aforementioned elements, particularly the escalating costs related to fertilizers and energy, as well as the ongoing challenges in sea freight operations which are likely to persist in the following months<sup>(</sup><span><sup>10</sup></span><sup>)</sup>.</p>","PeriodicalId":12404,"journal":{"name":"Food Science and Technology","volume":"38 3","pages":"36-39"},"PeriodicalIF":0.0000,"publicationDate":"2024-09-04","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/fsat.3803_9.x","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Food Science and Technology","FirstCategoryId":"97","ListUrlMain":"https://ifst.onlinelibrary.wiley.com/doi/10.1002/fsat.3803_9.x","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"Agricultural and Biological Sciences","Score":null,"Total":0}

引用次数: 0

Abstract

Maria Masoura outlines the drivers of supply chain disruption and their ripple effects on global food security.

The Food and Agriculture Organization (FAO) defines food security as when all people, at all times, have physical and economic access to sufficient safe and nutritious food that meets their dietary needs and food preferences for an active and healthy life. Currently, global food security is under pressure due to a combination of unprecedented pandemic threats and their consequences, climate change, economic disparities, and ongoing conflicts that strain supply chains and threaten the global integral right to food. The FAO, in conjunction with the World Food Programme (WFP), highlighted an intensifying crisis of food insecurity in their most recent Hunger Hotspots report, pinpointing eighteen areas of critical concern, with Mali, the Palestinian Territories, and (South) Sudan drawing particular attention. Haiti has been identified as a new area of concern due to escalating violence by non-state armed groups(1). The Integrated Food Security Phase Classification (IPC) has verified that in Gaza, 96% of the population, or approximately 2.15 million individuals, are grappling with severe food insecurity (at or above IPC Phase 3), and of these, 495,000 are enduring extreme food scarcity (IPC Phase 5) as projected through September 2024(2). The Agricultural Market Information System (AMIS) Market Monitor report from June 2024 has indicated that wheat yields are likely to be adversely affected by unfavourable climatic conditions, such as drought and extended periods of frost, particularly in pivotal agricultural regions of Russia. This situation is expected to lead to further escalations in prices, exacerbated by limitations in production and delays in transportation, especially within the Black Sea vicinity(3). In the wake of the ongoing Ukraine-Russia conflict, the global food crisis is worsened due to the growing number of food and fertilizer trade restrictions being put in place by countries to increase domestic supply and reduce prices. All these coupled with weather extremes, shipping delays, and relapsing pandemic waves further affect the already fragile food systems especially when limited substitutes exist for staple foods. This article provides an overview of the drivers of food insecurity and their direct consequences.

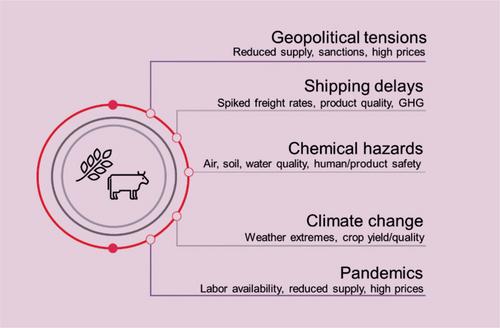

Rice, wheat, maize, and soybeans are the cornerstone crops of the global diet, accounting for nearly half of caloric intake, with rice and wheat alone making up 19% and 18%, respectively. A significant 60% of the world's food production occurs in just five countries: China, the United States, India, Brazil, and Argentina. Within these countries, certain areas are pivotal for production; for instance, five states in India are responsible for 88% of its wheat output, while 61% of the United States’ maize is produced by five states in the Midwest. This geographic concentration makes a substantial segment of the world's food supply susceptible to a range of factors that can disrupt the continuity of food production and distribution(4). Ukraine was known as the ‘breadbasket of Europe’ ranking among the top three global exporters of corn, wheat, barley, sunflower oil, and mineral fertilizers, while the developed agriculture made that country one of the top consumers of pesticides (around 125,000 tons a year). Geopolitical events (e.g. conflicts), climate extremes, pandemics, regulatory changes, sociological and technological pressures, economic factors (unemployment, rising food prices) growing inequality are among the most common drivers that put pressure on the supply chain and threaten global food security (Figure 1).

Worldwide, peace-making is in crisis and 2024 began with the ten active battlefields, among them: Gaza, Sudan, and Ukraine. The ‘paradigm’ of Russia's invasion of Ukraine is an unfortunate, still real scenario of how armed conflicts, including population displacement, destruction of food systems (e.g. land, infrastructure, etc.), and restricted humanitarian aid drive acute food insecurity in many geographical hotspots. As for today, the war in Ukraine, along with the ongoing issues in the Black Sea - a critical supply and transit hub for commodities and agricultural inputs – is having a significant economic and humanitarian impact. This situation is continuously getting worse due to the combined effects of weather extremes.

Since the onset of the war, Ukrainian farmers could not use their lands in occupied regions like Donetsk, Luhansk, Kherson, and Zaporizhzhia. Hence, production, trading, and supply of critical commodities (e.g. wheat, barley, sunflower oil) have been hampered. Ukraine, once a major supplier to the World Food Programme (WFP), now finds itself in need of assistance to meet its own food requirements. While several countries (e.g. US, UK, EU, Australia, Canada, and Japan) imposed sanctions on Russia, the latter found ways around such regimes and ’replied’ by embargoing exports of over 200 products (e.g. electronics, medical, agricultural, etc.) to nations it considers hostile, by shifting exports to China and India, redirecting its trade towards China and India, and closing the Nord Stream 1 pipeline, which was a primary source of Germany's natural gas. All that has made the import of crucial commodities (including oil, gas, fertilizers, and wheat) to the EU scarce and inflated prices while domestic food production slowed down in both the EU and China due to the record-high price of natural gas used to make fertilizers. Of note, fertilizer prices increased globally by 30% by early 2022 after experiencing an 80% hike in 2021 and the surging gas prices increased freight costs for all modes of transportation(5). This, in turn, caused delays and backlogs for industries, creating long and short-term ripples across supply chains, and affecting product quality.

Since the onset of the war, multiple attacks on the port of Odessa and sanctions on Russian vessels entering the UK, USA, and EU ports disrupted shipping, spiked freight rates, and suspended services to other longer sea routes. Upon the Middle East conflict, more attacks, on commercial vessels in the Red Sea region which extended to the Arabian Gulf, threatened oil shipments. Trading in the region of Israeli southern ports, especially Ashkelon and Ashdod faced heightened risk due to a missile attack and the closure of Ashkelon. Since November 2023, intensified assaults by Houthi forces on vessels destined for the Suez Canal have caused them to divert to a longer passage around the southern tip of Africa with multiple impacts such as rising costs, global delays and disruptions, and the increase of greenhouse gas (GHG) emissions. Russia also closed its airspace to European and U.S. airlines, forcing some long-haul flights to Asia to take longer routes (therefore increasing GHG emissions).

The contamination of air, water, livestock, and soil with munition debris, explosive remnants of war (ERW), and hazardous substances directly affects food safety and human health. Missile and air strikes in many parts of the country (Donetsk, Kharkiv, Chernihiv, Kyiv, Makariv, and Mariupol among them) resulted in massive widespread debris (e.g. asbestos used in more than 50% of infrastructure) while the supply of drinking water has been affected by hostilities in water pipelines and wastewater treatment stations. Potentially the most significant risk to humans is the exposure to chemical vapours (e.g. benzene, toluene, naphthalene, hydrogen sulphide, mercaptan, hydrocyanic acid, ammonia, PAHs, particulate matter, black carbon, aerosols, and a variety of gases, oils and fuel spills) resulted from fires/explosions to chemical industries and fuel infrastructure. Equally, munition debris (e.g. depleted uranium, explosives, heavy metals, unexploded ordnance, and landmines) contaminate agricultural land, drinking water, ecological habitats, flora, and fauna. Considering the fate of these harmful chemical deposits, ‘after-war’ agriculture in these fields is thought to be impossible to resume.

The ten warmest years in the 174-year record have all occurred during the last decade (2014–2023)(6). Crop production is highly sensitive to climate variability and is affected by weather extremes (e.g. temperature, heavy precipitation (including river floods), droughts, and storms (including tropical cyclones). Anthropogenic activity, particularly the expansion of crop and irrigation, industrialization, and transport (e.g. air/sea/land shipping), that increases GHG, and high aerosol concentrations, is the main driver of such phenomena. Although not all crops are equally vulnerable to climate change, increased atmospheric carbon dioxide (CO2), rising temperature, and changes in precipitation regimes, affect their yield, nutritional content, physical strength, and marketability. For instance, extended periods of drought can lead to crop failures. It is anticipated that C3 plants, when grown in environments with high CO2 concentrations, will exhibit reduced levels of proteins, minerals, and essential micronutrients like zinc and iron. Elevated temperatures can cause an uptick in respiration rates, which in turn diminishes the sugar content of the crops when harvested. Moreover, such climatic alterations make the crops more susceptible to pests and diseases, affecting them both in the fields and during storage. For example, plants that endure water saturation are more susceptible to viral infections, whereas those experiencing drought conditions struggle more to compete with weeds for soil moisture and nutrients(7).

High temperatures (average increase of 1.5°C) and low/unreliable rainfall will impact the global production of maize, rice, and potato which is expected to decrease in all breadbasket countries while utilization shows the opposite trend. For maize, the common responses to drought are a decrease in leaf number, abnormal root formation, slow growth rate, and lower chlorophyll content. In China, severe drought reduced maize yield by up to 14%(2).

The COVID-19 pandemic has doubled the severity of food insecurity, now affecting 811 million people worldwide. The crisis occurred initially due to the decline in food production and processing, limited access to critical inputs, and trade restrictions (e.g., transport delay of seeds and fertilizers slowed down the global agricultural process). Additionally, reduced labour (e.g., unemployment, social distancing measures, infections, and more limited transport systems) contributed to the instability, culminating in price surges even for staple foods.

This was compounded by the war in Ukraine that disrupted almost a third of the world's wheat market.

Geopolitical tensions, climate change, and extreme weather, all culminating in the wake of the pandemic, are tilting global food security into a high-risk state due to the vulnerability of staple food production, supply, and lack/limited substitutes. The ongoing conflicts in Ukraine and the Middle East battlefields have profound impacts on global food production and supplies, with far-reaching consequences for hunger and food security across the world. As of June 2024, 16 countries had implemented 22 food export bans, and 8 had implemented 15 export-limiting measures in major food commodities (e.g., wheat, soybean, rice, sugar, vegetable oils, etc.) while food inflation has increased between 5 and 30 per cent (or more) in most of the low- and middle-income countries(8). In particular, production and trade of wheat, maize, and rice in 2024 decreased and are forecast to decline below the 2023 level by 1.1 per cent. Further reductions in the crop yield are expected in light of La Niña (La Niña is also sometimes called El Viejo, or simply ‘a cold event’), predicted to dominate from August to October 2024 and persist through December 2024 to February 2025, which is thought to significantly change global weather patterns by influencing rainfall distribution and temperatures. Although it elevates the risk of flooding in vulnerable areas globally, it might also offer beneficial relief to certain regions, improving agricultural prospects(9).

FAO's 2024/2025 recent projections indicate a rise in production and an uptick in the final inventories of various staple commodities (Figure 2). Yet, the resilience of the global food production and distribution systems continues to be threatened by the aforementioned elements, particularly the escalating costs related to fertilizers and energy, as well as the ongoing challenges in sea freight operations which are likely to persist in the following months(10).

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们