{"title":"HQ controls, agency costs, and procedural justice","authors":"Erifili-Christina Chatzopoulou, Spyros Lioukas, Irini Voudouris","doi":"10.1002/gsj.1473","DOIUrl":null,"url":null,"abstract":"<div>\n \n \n <section>\n \n <h3> Research Summary</h3>\n \n <p>Monitoring, incentive alignment, and social controls are used to minimize the agency costs to headquarters (HQ) resulting from subsidiaries' opportunistic behaviors by aligning subsidiaries' behaviors and interests with those of the HQ. Subsidiaries' motivation to comply with these controls, however, is contingent on the social context that links the subsidiary to the HQ. In this context, we propose to identify procedural justice as a motivational contingency that shapes the conditions under which agency-driven controls can effectively minimize agency costs. Our results show that monitoring and social control reduce agency costs when procedural justice is high, whereas the use of incentive alignment mechanisms can have the opposite effect.</p>\n </section>\n \n <section>\n \n <h3> Managerial Summary</h3>\n \n <p>The headquarters (HQ) of multinational corporations use control mechanisms to ensure the alignment of their subsidiaries with the organization's interests and goals. However, these mechanisms do not always provide value to the corporation since subsidiaries may exhibit varying levels of motivation to comply with such controls, resulting in behaviors that range from resistance to compliance and ceremonial compliance to genuine compliance. We argue that the procedural justice applied by the HQ influences subsidiaries' motivation to comply with the controls implemented by the HQ. We find that in subsidiaries that operate in such a climate of fairness, monitoring based on rules, processes and procedures as well as social control can provide value, whereas the use of incentive alignment can lead to the opposite results.</p>\n </section>\n </div>","PeriodicalId":47563,"journal":{"name":"Global Strategy Journal","volume":"14 3","pages":"421-451"},"PeriodicalIF":4.7000,"publicationDate":"2023-02-27","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/gsj.1473","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Global Strategy Journal","FirstCategoryId":"91","ListUrlMain":"https://sms.onlinelibrary.wiley.com/doi/10.1002/gsj.1473","RegionNum":2,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS","Score":null,"Total":0}

引用次数: 0

Abstract

Research Summary

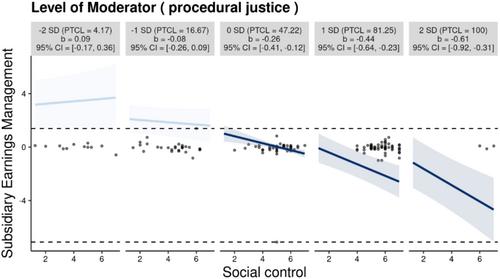

Monitoring, incentive alignment, and social controls are used to minimize the agency costs to headquarters (HQ) resulting from subsidiaries' opportunistic behaviors by aligning subsidiaries' behaviors and interests with those of the HQ. Subsidiaries' motivation to comply with these controls, however, is contingent on the social context that links the subsidiary to the HQ. In this context, we propose to identify procedural justice as a motivational contingency that shapes the conditions under which agency-driven controls can effectively minimize agency costs. Our results show that monitoring and social control reduce agency costs when procedural justice is high, whereas the use of incentive alignment mechanisms can have the opposite effect.

Managerial Summary

The headquarters (HQ) of multinational corporations use control mechanisms to ensure the alignment of their subsidiaries with the organization's interests and goals. However, these mechanisms do not always provide value to the corporation since subsidiaries may exhibit varying levels of motivation to comply with such controls, resulting in behaviors that range from resistance to compliance and ceremonial compliance to genuine compliance. We argue that the procedural justice applied by the HQ influences subsidiaries' motivation to comply with the controls implemented by the HQ. We find that in subsidiaries that operate in such a climate of fairness, monitoring based on rules, processes and procedures as well as social control can provide value, whereas the use of incentive alignment can lead to the opposite results.

期刊介绍:

The Global Strategy Journal is a premier platform dedicated to publishing highly influential managerially-oriented global strategy research worldwide. Covering themes such as international and global strategy, assembling the global enterprise, and strategic management, GSJ plays a vital role in advancing our understanding of global business dynamics.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们