{"title":"量化宽松政策的有效性:欧元私人资产的证据","authors":"Dimitris G. Kirikos","doi":"10.1111/boer.12427","DOIUrl":null,"url":null,"abstract":"<p>Proponents of quantitative easing (QE) unconventional policy have rather overstated some evidence that structural time series models do not predict long-term asset prices and yields as well as naive random walk forecasts, implying that predictions of price reversals cannot be profitable and, therefore, that QE effects are not transitory. Indeed, in this work we present evidence that naive models do not outperform structural vector autoregressive and Markov switching models in out-of-sample forecasting of corporate bond yields purchased by the European Central Bank, when the information set includes base money growth. It turns out that structural time series models provide additional information regarding the likelihood of price reversals, thus motivating investors to offset the effects of QE interventions if they perceive unconventional monetary policy regimes as temporary.</p>","PeriodicalId":46233,"journal":{"name":"Bulletin of Economic Research","volume":"76 2","pages":"354-370"},"PeriodicalIF":1.2000,"publicationDate":"2023-10-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/boer.12427","citationCount":"0","resultStr":"{\"title\":\"Quantitative easing effectiveness: Evidence from Euro private assets\",\"authors\":\"Dimitris G. Kirikos\",\"doi\":\"10.1111/boer.12427\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Proponents of quantitative easing (QE) unconventional policy have rather overstated some evidence that structural time series models do not predict long-term asset prices and yields as well as naive random walk forecasts, implying that predictions of price reversals cannot be profitable and, therefore, that QE effects are not transitory. Indeed, in this work we present evidence that naive models do not outperform structural vector autoregressive and Markov switching models in out-of-sample forecasting of corporate bond yields purchased by the European Central Bank, when the information set includes base money growth. It turns out that structural time series models provide additional information regarding the likelihood of price reversals, thus motivating investors to offset the effects of QE interventions if they perceive unconventional monetary policy regimes as temporary.</p>\",\"PeriodicalId\":46233,\"journal\":{\"name\":\"Bulletin of Economic Research\",\"volume\":\"76 2\",\"pages\":\"354-370\"},\"PeriodicalIF\":1.2000,\"publicationDate\":\"2023-10-19\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/boer.12427\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Bulletin of Economic Research\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/boer.12427\",\"RegionNum\":4,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Bulletin of Economic Research","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/boer.12427","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

Quantitative easing effectiveness: Evidence from Euro private assets

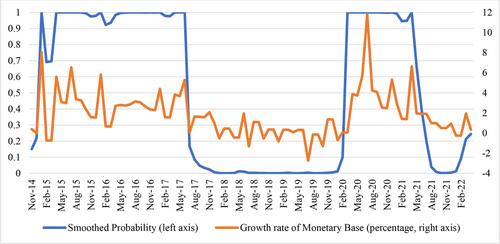

Proponents of quantitative easing (QE) unconventional policy have rather overstated some evidence that structural time series models do not predict long-term asset prices and yields as well as naive random walk forecasts, implying that predictions of price reversals cannot be profitable and, therefore, that QE effects are not transitory. Indeed, in this work we present evidence that naive models do not outperform structural vector autoregressive and Markov switching models in out-of-sample forecasting of corporate bond yields purchased by the European Central Bank, when the information set includes base money growth. It turns out that structural time series models provide additional information regarding the likelihood of price reversals, thus motivating investors to offset the effects of QE interventions if they perceive unconventional monetary policy regimes as temporary.

期刊介绍:

The Bulletin of Economic Research is an international journal publishing articles across the entire field of economics, econometrics and economic history. The Bulletin contains original theoretical, applied and empirical work which makes a substantial contribution to the subject and is of broad interest to economists. We welcome submissions in all fields and, with the Bulletin expanding in new areas, we particularly encourage submissions in the fields of experimental economics, financial econometrics and health economics. In addition to full-length articles the Bulletin publishes refereed shorter articles, notes and comments; authoritative survey articles in all areas of economics and special themed issues.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们