{"title":"投资组合优化问题中的信息测量比较研究","authors":"Luckshay Batra, H. C. Taneja","doi":"10.1007/s12652-024-04766-2","DOIUrl":null,"url":null,"abstract":"<p>This paper presents a rich class of information theoretical measures designed to enhance the accuracy of portfolio risk assessments. The Mean-Variance model, pioneered by Harry Markowitz, revolutionized the financial sector as the first formal mathematical method to risk-averse investing in portfolio optimization theory. We analyze the effectiveness of this with the models that replace expected portfolio variance with measures of information (uncertainty of the portfolio allocations to the different assets) and five major practical issues. The empirical analysis is carried out on the historical data of Indian financial stock indices by application of portfolio optimization problem with information measures as the objective function and constraints derived from the return and the risk. Our findings indicate that the information measures with parameters can be used as an adequate supplement to traditional portfolio optimization models such as the mean-variance model.</p>","PeriodicalId":14959,"journal":{"name":"Journal of Ambient Intelligence and Humanized Computing","volume":"14 1","pages":""},"PeriodicalIF":0.0000,"publicationDate":"2024-03-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Comparative study of information measures in portfolio optimization problems\",\"authors\":\"Luckshay Batra, H. C. Taneja\",\"doi\":\"10.1007/s12652-024-04766-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper presents a rich class of information theoretical measures designed to enhance the accuracy of portfolio risk assessments. The Mean-Variance model, pioneered by Harry Markowitz, revolutionized the financial sector as the first formal mathematical method to risk-averse investing in portfolio optimization theory. We analyze the effectiveness of this with the models that replace expected portfolio variance with measures of information (uncertainty of the portfolio allocations to the different assets) and five major practical issues. The empirical analysis is carried out on the historical data of Indian financial stock indices by application of portfolio optimization problem with information measures as the objective function and constraints derived from the return and the risk. Our findings indicate that the information measures with parameters can be used as an adequate supplement to traditional portfolio optimization models such as the mean-variance model.</p>\",\"PeriodicalId\":14959,\"journal\":{\"name\":\"Journal of Ambient Intelligence and Humanized Computing\",\"volume\":\"14 1\",\"pages\":\"\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2024-03-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Ambient Intelligence and Humanized Computing\",\"FirstCategoryId\":\"94\",\"ListUrlMain\":\"https://doi.org/10.1007/s12652-024-04766-2\",\"RegionNum\":3,\"RegionCategory\":\"计算机科学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"Computer Science\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Ambient Intelligence and Humanized Computing","FirstCategoryId":"94","ListUrlMain":"https://doi.org/10.1007/s12652-024-04766-2","RegionNum":3,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"Computer Science","Score":null,"Total":0}

Comparative study of information measures in portfolio optimization problems

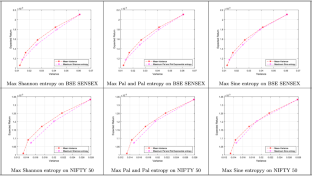

This paper presents a rich class of information theoretical measures designed to enhance the accuracy of portfolio risk assessments. The Mean-Variance model, pioneered by Harry Markowitz, revolutionized the financial sector as the first formal mathematical method to risk-averse investing in portfolio optimization theory. We analyze the effectiveness of this with the models that replace expected portfolio variance with measures of information (uncertainty of the portfolio allocations to the different assets) and five major practical issues. The empirical analysis is carried out on the historical data of Indian financial stock indices by application of portfolio optimization problem with information measures as the objective function and constraints derived from the return and the risk. Our findings indicate that the information measures with parameters can be used as an adequate supplement to traditional portfolio optimization models such as the mean-variance model.

期刊介绍:

The purpose of JAIHC is to provide a high profile, leading edge forum for academics, industrial professionals, educators and policy makers involved in the field to contribute, to disseminate the most innovative researches and developments of all aspects of ambient intelligence and humanized computing, such as intelligent/smart objects, environments/spaces, and systems. The journal discusses various technical, safety, personal, social, physical, political, artistic and economic issues. The research topics covered by the journal are (but not limited to):

Pervasive/Ubiquitous Computing and Applications

Cognitive wireless sensor network

Embedded Systems and Software

Mobile Computing and Wireless Communications

Next Generation Multimedia Systems

Security, Privacy and Trust

Service and Semantic Computing

Advanced Networking Architectures

Dependable, Reliable and Autonomic Computing

Embedded Smart Agents

Context awareness, social sensing and inference

Multi modal interaction design

Ergonomics and product prototyping

Intelligent and self-organizing transportation networks & services

Healthcare Systems

Virtual Humans & Virtual Worlds

Wearables sensors and actuators

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们