{"title":"揭示科维德-19 大流行病期间印度股票行业的非对称回报溢出效应及投资组合影响","authors":"Aswini Kumar Mishra, Kamesh Anand K, Akhil Venkatasai Kappagantula","doi":"10.1016/j.najef.2024.102297","DOIUrl":null,"url":null,"abstract":"<div><div>This paper aims to provide a systematic inquiry into the return spillover dynamics between a network of Indian sectoral indices during the pre- and post-pandemic periods. To analyze the same, this paper uses the asymmetric time-varying parameter vector autoregressions (TVP-VAR) framework. Furthermore, in the spirit of Broadstock et al. (2020), we perform dynamic portfolio exercises based on common hedging techniques and the minimum connectedness portfolio approach to determine what better captures asymmetry. Our daily dataset includes 12 sectoral stocks spanning from January 01, 2017, to May 5, 2023. The findings reveal that negative connectedness dominates throughout the sample period, demonstrating that profit-maximizing agents and risk-averse investors are more likely to react negatively to news. We also show that in the network, the average net transmitters are the banking and other financial service sectors, whereas the net receivers are the information technology, pharmaceutical, and fast-moving consumer goods sectors throughout the period under consideration. Our results show that the minimum connectedness portfolio (MCoP) approach is a very useful method based on Sharpe ratios, as it is either the first or second most profitable among these three competing methods. These results, therefore, yield valuable insights for policymakers and investors.</div></div>","PeriodicalId":47831,"journal":{"name":"North American Journal of Economics and Finance","volume":"75 ","pages":"Article 102297"},"PeriodicalIF":3.9000,"publicationDate":"2025-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Unveiling asymmetric return spillovers with portfolio implications among Indian stock sectors during Covid-19 pandemic\",\"authors\":\"Aswini Kumar Mishra, Kamesh Anand K, Akhil Venkatasai Kappagantula\",\"doi\":\"10.1016/j.najef.2024.102297\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><div>This paper aims to provide a systematic inquiry into the return spillover dynamics between a network of Indian sectoral indices during the pre- and post-pandemic periods. To analyze the same, this paper uses the asymmetric time-varying parameter vector autoregressions (TVP-VAR) framework. Furthermore, in the spirit of Broadstock et al. (2020), we perform dynamic portfolio exercises based on common hedging techniques and the minimum connectedness portfolio approach to determine what better captures asymmetry. Our daily dataset includes 12 sectoral stocks spanning from January 01, 2017, to May 5, 2023. The findings reveal that negative connectedness dominates throughout the sample period, demonstrating that profit-maximizing agents and risk-averse investors are more likely to react negatively to news. We also show that in the network, the average net transmitters are the banking and other financial service sectors, whereas the net receivers are the information technology, pharmaceutical, and fast-moving consumer goods sectors throughout the period under consideration. Our results show that the minimum connectedness portfolio (MCoP) approach is a very useful method based on Sharpe ratios, as it is either the first or second most profitable among these three competing methods. These results, therefore, yield valuable insights for policymakers and investors.</div></div>\",\"PeriodicalId\":47831,\"journal\":{\"name\":\"North American Journal of Economics and Finance\",\"volume\":\"75 \",\"pages\":\"Article 102297\"},\"PeriodicalIF\":3.9000,\"publicationDate\":\"2025-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"North American Journal of Economics and Finance\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://www.sciencedirect.com/science/article/pii/S1062940824002225\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2024/10/16 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"North American Journal of Economics and Finance","FirstCategoryId":"96","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S1062940824002225","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2024/10/16 0:00:00","PubModel":"Epub","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Unveiling asymmetric return spillovers with portfolio implications among Indian stock sectors during Covid-19 pandemic

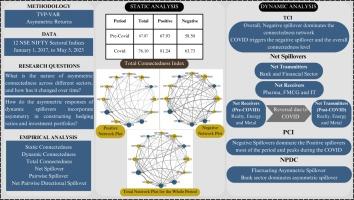

This paper aims to provide a systematic inquiry into the return spillover dynamics between a network of Indian sectoral indices during the pre- and post-pandemic periods. To analyze the same, this paper uses the asymmetric time-varying parameter vector autoregressions (TVP-VAR) framework. Furthermore, in the spirit of Broadstock et al. (2020), we perform dynamic portfolio exercises based on common hedging techniques and the minimum connectedness portfolio approach to determine what better captures asymmetry. Our daily dataset includes 12 sectoral stocks spanning from January 01, 2017, to May 5, 2023. The findings reveal that negative connectedness dominates throughout the sample period, demonstrating that profit-maximizing agents and risk-averse investors are more likely to react negatively to news. We also show that in the network, the average net transmitters are the banking and other financial service sectors, whereas the net receivers are the information technology, pharmaceutical, and fast-moving consumer goods sectors throughout the period under consideration. Our results show that the minimum connectedness portfolio (MCoP) approach is a very useful method based on Sharpe ratios, as it is either the first or second most profitable among these three competing methods. These results, therefore, yield valuable insights for policymakers and investors.

期刊介绍:

The focus of the North-American Journal of Economics and Finance is on the economics of integration of goods, services, financial markets, at both regional and global levels with the role of economic policy in that process playing an important role. Both theoretical and empirical papers are welcome. Empirical and policy-related papers that rely on data and the experiences of countries outside North America are also welcome. Papers should offer concrete lessons about the ongoing process of globalization, or policy implications about how governments, domestic or international institutions, can improve the coordination of their activities. Empirical analysis should be capable of replication. Authors of accepted papers will be encouraged to supply data and computer programs.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们