{"title":"具有协变量测量误差的高维稀疏加性风险回归的双偏置校正。","authors":"Xiaobo Wang, Jiayu Huang, Guosheng Yin, Jian Huang, Yuanshan Wu","doi":"10.1007/s10985-022-09568-2","DOIUrl":null,"url":null,"abstract":"<p><p>We propose an inferential procedure for additive hazards regression with high-dimensional survival data, where the covariates are prone to measurement errors. We develop a double bias correction method by first correcting the bias arising from measurement errors in covariates through an estimating function for the regression parameter. By adopting the convex relaxation technique, a regularized estimator for the regression parameter is obtained by elaborately designing a feasible loss based on the estimating function, which is solved via linear programming. Using the Neyman orthogonality, we propose an asymptotically unbiased estimator which further corrects the bias caused by the convex relaxation and regularization. We derive the convergence rate of the proposed estimator and establish the asymptotic normality for the low-dimensional parameter estimator and the linear combination thereof, accompanied with a consistent estimator for the variance. Numerical experiments are carried out on both simulated and real datasets to demonstrate the promising performance of the proposed double bias correction method.</p>","PeriodicalId":49908,"journal":{"name":"Lifetime Data Analysis","volume":"29 1","pages":"115-141"},"PeriodicalIF":1.0000,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Double bias correction for high-dimensional sparse additive hazards regression with covariate measurement errors.\",\"authors\":\"Xiaobo Wang, Jiayu Huang, Guosheng Yin, Jian Huang, Yuanshan Wu\",\"doi\":\"10.1007/s10985-022-09568-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>We propose an inferential procedure for additive hazards regression with high-dimensional survival data, where the covariates are prone to measurement errors. We develop a double bias correction method by first correcting the bias arising from measurement errors in covariates through an estimating function for the regression parameter. By adopting the convex relaxation technique, a regularized estimator for the regression parameter is obtained by elaborately designing a feasible loss based on the estimating function, which is solved via linear programming. Using the Neyman orthogonality, we propose an asymptotically unbiased estimator which further corrects the bias caused by the convex relaxation and regularization. We derive the convergence rate of the proposed estimator and establish the asymptotic normality for the low-dimensional parameter estimator and the linear combination thereof, accompanied with a consistent estimator for the variance. Numerical experiments are carried out on both simulated and real datasets to demonstrate the promising performance of the proposed double bias correction method.</p>\",\"PeriodicalId\":49908,\"journal\":{\"name\":\"Lifetime Data Analysis\",\"volume\":\"29 1\",\"pages\":\"115-141\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2023-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Lifetime Data Analysis\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://doi.org/10.1007/s10985-022-09568-2\",\"RegionNum\":3,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Lifetime Data Analysis","FirstCategoryId":"100","ListUrlMain":"https://doi.org/10.1007/s10985-022-09568-2","RegionNum":3,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

Double bias correction for high-dimensional sparse additive hazards regression with covariate measurement errors.

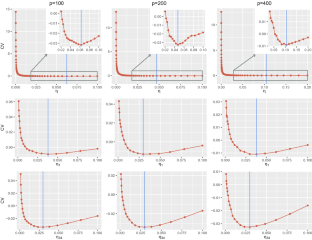

We propose an inferential procedure for additive hazards regression with high-dimensional survival data, where the covariates are prone to measurement errors. We develop a double bias correction method by first correcting the bias arising from measurement errors in covariates through an estimating function for the regression parameter. By adopting the convex relaxation technique, a regularized estimator for the regression parameter is obtained by elaborately designing a feasible loss based on the estimating function, which is solved via linear programming. Using the Neyman orthogonality, we propose an asymptotically unbiased estimator which further corrects the bias caused by the convex relaxation and regularization. We derive the convergence rate of the proposed estimator and establish the asymptotic normality for the low-dimensional parameter estimator and the linear combination thereof, accompanied with a consistent estimator for the variance. Numerical experiments are carried out on both simulated and real datasets to demonstrate the promising performance of the proposed double bias correction method.

期刊介绍:

The objective of Lifetime Data Analysis is to advance and promote statistical science in the various applied fields that deal with lifetime data, including: Actuarial Science – Economics – Engineering Sciences – Environmental Sciences – Management Science – Medicine – Operations Research – Public Health – Social and Behavioral Sciences.

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们