{"title":"纳税申报信息对股权投资者有用吗?","authors":"Paul Demeré","doi":"10.1007/s11142-023-09792-7","DOIUrl":null,"url":null,"abstract":"Abstract I examine whether tax return information is useful to equity investors. I do so indirectly, by exploiting unique features of the syndicated loan market, as evidence shows that lenders obtain tax returns from borrowers and that lenders’ private information is transmitted to equity markets when institutional investors are part of a loan syndicate. I find significant increases in tax expense valuation and decreases in tax-related market anomalies following the issuance of institutional syndicated loans, suggesting that equity investors find information about firm performance in tax returns that is useful for their trading decisions. I also find evidence suggesting that institutional investors may determine their loan syndicate participation in part based on the value of tax return information. This study extends prior research and informs policy debates over public disclosure of corporate tax return information by providing evidence to support that tax returns can be useful to investor decision making.","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"112 1","pages":"0"},"PeriodicalIF":4.8000,"publicationDate":"2023-08-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"1","resultStr":"{\"title\":\"Is tax return information useful to equity investors?\",\"authors\":\"Paul Demeré\",\"doi\":\"10.1007/s11142-023-09792-7\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"Abstract I examine whether tax return information is useful to equity investors. I do so indirectly, by exploiting unique features of the syndicated loan market, as evidence shows that lenders obtain tax returns from borrowers and that lenders’ private information is transmitted to equity markets when institutional investors are part of a loan syndicate. I find significant increases in tax expense valuation and decreases in tax-related market anomalies following the issuance of institutional syndicated loans, suggesting that equity investors find information about firm performance in tax returns that is useful for their trading decisions. I also find evidence suggesting that institutional investors may determine their loan syndicate participation in part based on the value of tax return information. This study extends prior research and informs policy debates over public disclosure of corporate tax return information by providing evidence to support that tax returns can be useful to investor decision making.\",\"PeriodicalId\":48120,\"journal\":{\"name\":\"Review of Accounting Studies\",\"volume\":\"112 1\",\"pages\":\"0\"},\"PeriodicalIF\":4.8000,\"publicationDate\":\"2023-08-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Review of Accounting Studies\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s11142-023-09792-7\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11142-023-09792-7","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Is tax return information useful to equity investors?

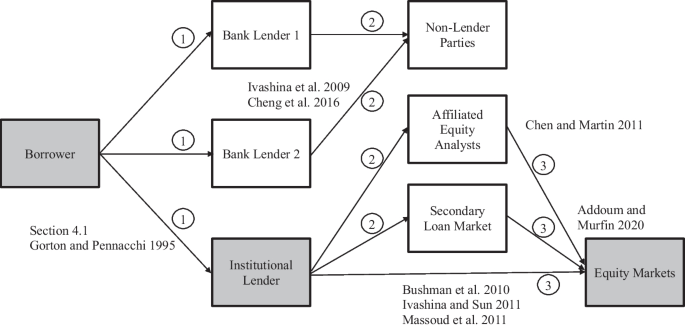

Abstract I examine whether tax return information is useful to equity investors. I do so indirectly, by exploiting unique features of the syndicated loan market, as evidence shows that lenders obtain tax returns from borrowers and that lenders’ private information is transmitted to equity markets when institutional investors are part of a loan syndicate. I find significant increases in tax expense valuation and decreases in tax-related market anomalies following the issuance of institutional syndicated loans, suggesting that equity investors find information about firm performance in tax returns that is useful for their trading decisions. I also find evidence suggesting that institutional investors may determine their loan syndicate participation in part based on the value of tax return information. This study extends prior research and informs policy debates over public disclosure of corporate tax return information by providing evidence to support that tax returns can be useful to investor decision making.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们