Christopher Armstrong, Jacky Chau, Christopher D. Ittner, Jason J. Xiao

{"title":"每股收益目标和首席执行官激励机制","authors":"Christopher Armstrong, Jacky Chau, Christopher D. Ittner, Jason J. Xiao","doi":"10.1007/s11142-023-09815-3","DOIUrl":null,"url":null,"abstract":"<p>We examine differences in CEOs’ achievement of earnings per share (EPS) targets related to (1) analysts’ forecasts and (2) internal cash bonus payouts. Our focus on firms with <i>different benchmarks</i> for the <i>same performance metric</i> enables us to assess the relative importance of the incentives that each EPS target provides based on its revealed achievement. Most CEOs meet analysts’ final consensus EPS forecasts but are unlikely to meet bonus EPS targets that exceed forecasted EPS. Nearly all CEOs receive some EPS-based cash bonus, even when missing the forecast. Moreover, CEOs with bonus targets that are easier to achieve than the consensus forecast tend to receive <i>more</i> annual pay, suggesting that boards often set more achievable EPS targets to provide extra compensation to CEOs while maintaining the appearance of pay-for-performance. Our results highlight the importance of considering both types of EPS targets simultaneously when assessing their respective incentive properties.</p>","PeriodicalId":48120,"journal":{"name":"Review of Accounting Studies","volume":"9 1","pages":""},"PeriodicalIF":5.8000,"publicationDate":"2024-01-22","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Earnings per share targets and CEO incentives\",\"authors\":\"Christopher Armstrong, Jacky Chau, Christopher D. Ittner, Jason J. Xiao\",\"doi\":\"10.1007/s11142-023-09815-3\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We examine differences in CEOs’ achievement of earnings per share (EPS) targets related to (1) analysts’ forecasts and (2) internal cash bonus payouts. Our focus on firms with <i>different benchmarks</i> for the <i>same performance metric</i> enables us to assess the relative importance of the incentives that each EPS target provides based on its revealed achievement. Most CEOs meet analysts’ final consensus EPS forecasts but are unlikely to meet bonus EPS targets that exceed forecasted EPS. Nearly all CEOs receive some EPS-based cash bonus, even when missing the forecast. Moreover, CEOs with bonus targets that are easier to achieve than the consensus forecast tend to receive <i>more</i> annual pay, suggesting that boards often set more achievable EPS targets to provide extra compensation to CEOs while maintaining the appearance of pay-for-performance. Our results highlight the importance of considering both types of EPS targets simultaneously when assessing their respective incentive properties.</p>\",\"PeriodicalId\":48120,\"journal\":{\"name\":\"Review of Accounting Studies\",\"volume\":\"9 1\",\"pages\":\"\"},\"PeriodicalIF\":5.8000,\"publicationDate\":\"2024-01-22\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Review of Accounting Studies\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://doi.org/10.1007/s11142-023-09815-3\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Review of Accounting Studies","FirstCategoryId":"91","ListUrlMain":"https://doi.org/10.1007/s11142-023-09815-3","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

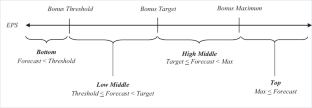

We examine differences in CEOs’ achievement of earnings per share (EPS) targets related to (1) analysts’ forecasts and (2) internal cash bonus payouts. Our focus on firms with different benchmarks for the same performance metric enables us to assess the relative importance of the incentives that each EPS target provides based on its revealed achievement. Most CEOs meet analysts’ final consensus EPS forecasts but are unlikely to meet bonus EPS targets that exceed forecasted EPS. Nearly all CEOs receive some EPS-based cash bonus, even when missing the forecast. Moreover, CEOs with bonus targets that are easier to achieve than the consensus forecast tend to receive more annual pay, suggesting that boards often set more achievable EPS targets to provide extra compensation to CEOs while maintaining the appearance of pay-for-performance. Our results highlight the importance of considering both types of EPS targets simultaneously when assessing their respective incentive properties.

期刊介绍:

Review of Accounting Studies provides an outlet for significant academic research in accounting including theoretical, empirical, and experimental work. The journal is committed to the principle that distinctive scholarship is rigorous. While the editors encourage all forms of research, it must contribute to the discipline of accounting. The Review of Accounting Studies is committed to prompt turnaround on the manuscripts it receives. For the majority of manuscripts the journal will make an accept-reject decision on the first round. Authors will be provided the opportunity to revise accepted manuscripts in response to reviewer and editor comments; however, discretion over such manuscripts resides principally with the authors. An editorial revise and resubmit decision is reserved for new submissions which are not acceptable in their current version, but for which the editor sees a clear path of changes which would make the manuscript publishable. Officially cited as: Rev Account Stud

分享

分享

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: 扫码关注我们

扫码关注我们